LONG $CTLP - Cantaloupe, Inc.

A Profitable, Underappreciated Fintech Leader in Unattended Retail

Cantaloupe, Inc.

NASDAQGS: CTLP | 01/17/2025

Cantaloupe provides self-service commerce software and payment solutions, integrating telematics to power transactions across unattended retail formats. The company serves over 32,000 customers who operate 1.23M active devices. Of these, 60% are deployed within enterprise accounts and 40% within SMBs, collectively processing over $3B in annual transaction volume. CTLP’s value proposition offers customers a 20-35% revenue lift and a 30-40% reduction in OpEx upon full onboarding to the platform.

The company estimates its TAM at $6.4B ($3.8B in North America), growing at a 10% CAGR. While historically focused on F&B vending, the industry is rapidly expanding into micro markets and smart stores, where CTLP has positioned itself as a leader. The market remains fragmented, with key competitors including Nayax (NYAX), a direct competitor operating across 40 verticals compared to CTLP’s 8, and Crane NXT (CXT), which has a broader product portfolio and is not a pure-play competitor.

CTLP generates revenue from transaction fees (58%), subscription fees (28%), and equipment sales (14%). Management is focused on profitable growth by expanding transaction margins as the average ticket size increases and prioritizing higher-margin subscription revenue, particularly from its cloud-based ERP software (Seed) and equipment-bundled subscriptions. The strategic shift to bundling hardware rentals with SaaS under the Cantaloupe ONE program allows CTLP to charge a premium on hardware while driving recurring, high-margin SaaS revenue (~88–90% gross margin), improving overall profitability compared to its previous reliance on equipment sales. Key growth initiatives include international expansion into Europe and Latin America and increased penetration into high-ticket verticals like entertainment and gaming.

Cantaloupe has undergone a significant turnaround since its rebranding from USA Technologies. After facing severe accounting issues that led to a temporary delisting in 2019, activist investor Hudson Executive Capital overhauled the board and management. Under the leadership of the current CEO, appointed in February 2022, Cantaloupe has transitioned from a recovery phase to a focus on profitable growth.

At its 2022 Investor Day, management outlined a three-year plan projecting a 15% revenue CAGR through 2026, driven by a 20% CAGR in subscription revenue. Since then, CTLP has outperformed on transaction revenues but underperformed on subscription revenues, primarily due to challenges in addressing the backlog of sold equipment and delays in activation timelines, caused by a lack of installers and insufficient customer activation training. FY24 revenue growth was also negatively impacted by the lapping effect of the 3G to 4G upgrade cycle in FY23 resulting in a -14.6% decline in FY24 equipment sales. In Q4’24, management revised its growth expectations, forecasting subscription revenue growth to reaccelerate to 15%+ and continued outperformance in transaction revenues at 18%+, with Adj. EBITDA expected to reach $75M at a 20% margin by FY26.

In my view, supported by a flurry of recent insider purchases that align with management’s confidence, CTLP is well positioned to achieve its FY26 Adj. EBITDA target, with multiple levers for outperformance on both the top and bottom lines relative to consensus estimates.

Key Thesis Points:

1. Increased adoption of micro-markets and smart stores, along with, expansion into high-ticket verticals like entertainment and gaming are poised to deliver strong subscription and transaction fee growth

2. International expansion is overlooked, with significant revenue potential in untapped markets.

3. Incremental margins are underappreciated by the market.

1. Increased adoption of micro-markets and smart stores, along with, expansion into high-ticket verticals like entertainment and gaming are poised to deliver strong subscription and transaction fee growth

Smart stores and micro-markets have become a key focus for CTLP. A smart store is a compact, enclosed supermarket equipped with technology that tracks inventory and reduces theft by requiring a payment method—such as a credit card tap—before the door opens. These stores are ideal for high-traffic areas where security is a concern. In contrast, micro-markets function as smaller, unmanned convenience stores featuring open shelves, fresh food, beverages, and self-checkout kiosks. Typically located in employee breakrooms and other restricted-access environments like corporate offices, hospitals, luxury car dealerships, and high-end residential complexes, micro-markets benefit from a predictable, recurring customer base with minimal theft risk.

Advanced features like smart locks and sophisticated cooling systems in these setups allow merchants to offer premium products beyond traditional vending fare, significantly boosting average transaction sizes. In 2024, the average ticket size in micro-markets and smart stores reached $3.19—30% higher than the $2.45 average in traditional vending—and customers spent 50% more in these formats due to their convenience. In Q4’23, management noted that micro-markets accounted for well below 10% of revenues, but they expect this share to grow to 25–30% over the next 3–5 years (FY26–FY28). Although subsequent updates have not provided a detailed revenue breakdown, the increasing average ticket size and positive commentary suggest that micro-markets should contribute at least 10% of revenues by FY25—approximately $31.4M in my base case scenario. With an anticipated CAGR of 58%, this segment is projected to represent 25% of total revenues, or about $122.9M, by FY28.

CTLP is also expanding into high-ticket verticals such as entertainment and gaming. With the acquisition of Cheq, the company has opened doors to sports stadiums and other entertainment venues for its POS payment processing and ERP software solutions, addressing on-premises F&B and merchandise needs. For example, the San Jose Earthquakes’ PayPal Park stadium, which has a capacity of 18,000, began using these solutions in December 2024, where average in-stadium transaction sizes reach around $30. Additionally, CTLP is targeting the amusement industry with its Engage Pulse card readers designed for arcades. In this sector, the ease of playing multiple rounds through cashless transactions leads to an average ticket size of $6.13—about 750% higher than the $0.81 for cash transactions—and these cashless transactions account for approximately 63% of total sales volume, further underscoring the significant revenue potential in these environments.

CTLP’s transaction fees revenue model relies on three key drivers: the total number of transactions, the average ticket size, and the transaction take rate. Total dollar volume is determined by multiplying the number of transactions by the average ticket size, with the transaction take rate applied to derive transaction revenues.

In my base case model, I project total transactions to grow 4.5% Y/Y in FY25, with 0.5% incremental increases through FY27—conservative compared to the industry’s forecasted 5-8% CAGR for self-service commerce transactions. CTLP’s position is notable for its rising take rate from transaction dollar volumes, reflecting greater monetization of processed transactions. Take rates increased from 4.84% in FY22 to 5.27% in Q1’25, driven by higher-ticket items enabled by CTLP’s success with micro markets, smart stores, and expansion into verticals like amusement and sports. In contrast, Nayax, operating in lower-ticket verticals, reports a take rate of just 2.75% (Q3’24). While management expects take rates to stabilize at 5.27% in FY25, I see upside to 5.32% by FY26, supported by vertical-specific card readers and kiosks in amusement and sports, along with continued expansion of micro-markets and smart stores in premium locations like luxury residences. Similarly, I expect the average ticket size to grow 11% in FY25, 12% in FY26, and 12.5% in FY27 and FY28, driven by increasing adoption of micro-markets, smart stores, and high-ticket verticals. The table below presents a breakdown of the average ticket size across vending and low-ticket verticals, micro-markets and smart stores, and other high-ticket verticals such as entertainment and gaming.

As a result of the drivers outlined above, base case transaction fees are projected to grow at an 18.75% CAGR from FY25 to FY28:

Cantaloupe’s subscription fees benefit directly from the growth of micro-markets and smart stores. As highlighted on an earnings call: “People are buying $10 salads instead of a $1 candy bar. And oh, yes, by the way, that helps us sell Seed (software) because salad’s really good for a couple of days. So having an inventory system that can manage that is very beneficial.” Micro-markets typically have a 100% software attach rate, reflecting their need for inventory management, sales tracking, and dynamic pricing. Beyond micro-markets, Cheq’s event management software, which includes mobile ordering, drives subscription growth as CTLP signs more sports clients for POS payment processing. Additionally, the Cantaloupe ONE program, integrating vending machines in stadiums and entertainment venues, expands cross-selling opportunities. Clients in these verticals can also adopt SEED software for inventory management, predictive analytics, and route scheduling, strengthening recurring revenue streams.

CTLP’s subscription fee revenue model depends on two key drivers: active devices and subscription fees per active device. My base case projects active devices to grow at a steady +5% Y/Y from FY25–FY28, bolstered by international expansion and micro-market deployments. Notably, micro-markets typically incorporate 2-3x the number of devices found in traditional vending machine settings—such as refrigerated units, card readers, and, in some cases, multiple self-serve kiosks. Subscription fees per active device consist of equipment rental and software fees. I expect subscription fees per active device to rebound from FY24’s 6.4% Y/Y growth to 10% Y/Y in FY25. This improvement is driven by resolved installation and activation bottlenecks and increased software attach rates. Moreover, significant upfront CapEx for micro-market customers—typically $4,000 to $6,000 for items like kiosks and coolers—makes the bundled hardware and SaaS solution under the Cantaloupe ONE program more appealing. As of Q1’25, deployment and activation timelines have normalized to six weeks, indicating easing backlogs and suggesting that overall subscription revenue growth could reaccelerate to over 15% (up from 10.2% in FY24). As a result of the drivers laid out above, I project overall subscription fees to grow at a 16.3% CAGR from FY25-FY28:

2. International expansion is overlooked, with significant revenue potential in untapped markets.

CTLP reinforced its international expansion strategy in December 2022 with the acquisition of 32M, broadening its presence in Europe and North America and enabling an immediate cross-sell to 32M’s 3,000 customers via an existing integration. In Q4’24, CTLP further expanded internationally with the acquisition of SB Software, a UK- and Ireland-based provider of vending and coffee management software with over 30,000 subscriptions. This deal not only added coffee management software capabilities to CTLP’s platform but also created cross-selling opportunities for its payment processing services. While both acquisitions are long-term growth drivers, their near-term impact remains limited—32M is expected to generate ~$20M in FY25 revenue (25% ex-North America) at a 20% EBITDA margin, while SB Software’s contribution remains <1% of total revenue. My base case assumes no further acquisitions, though additional deals are likely as industry consolidation accelerates.

CTLP’s organic international expansion continues to gain momentum across the EU and LatAm. In the UK, Decorum Vending recently installed 630 vending machines in high-traffic areas, while in Mexico, a strategic partnership with one of the country’s largest operators resulted in the deployment of 4,000 devices under the Cantaloupe ONE program. Additionally, CTLP completed the internationalization of its SEED software, opening up new subscription revenue opportunities in Latin America. International revenue is estimated to have represented 5% of total revenue ($13.4M) in FY24, and I estimate it will grow to $49M (10% of total revenue) by FY28, reflecting a 38% CAGR. These projections remain conservative given the expansive TAM outside North America, particularly in LatAm, where the market remains largely untapped.

3. Incremental margins are underappreciated by the market

CTLP demonstrates strong operating leverage, with Adj. EBITDA growing at an 85% CAGR from FY22-FY24. However, the market undervalues its profitability potential and underestimates management's ability to reach its FY26 Adj. EBITDA target of $75M. This skepticism stems from the company’s historical lack of earnings and the perception that transaction gross margins, a major contributor to EBITDA, come from a commoditized business. Additionally, the market had initially expected subscription gross margins to be the primary driver, with subscription revenue growing at an expected 20% Y/Y, but this target has now been revised down to 15%+. These perceptions overlook CTLP’s near-zero customer churn, the highly recurring nature of its transaction fees, and the structural advantage of increasing software attach rates—albeit at a slower pace—which strengthens retention by raising switching costs.

CTLP’s transaction business benefits from high operating leverage, with its payment infrastructure able to handle incremental transaction volume without a proportional increase in fixed costs. The rising average ticket size, the rising transaction take rate, and negotiation with third-party payment processor rates along with fixed cost operating leverage have contributed to driving transaction margins from 16% in FY23 to 21% in FY24. Management expects transaction margins to improve significantly as average ticket sizes grow and operating leverage benefits kick in from the fixed portion of processing fees.

Transaction gross margins, now a key EBITDA driver, are expected to grow at a steady +4% Y/Y, reaching 37.1% in FY28—a fairly conservative assumption, sitting at the low end of gross margins observed in the average payments company (30-60%). This growth is driven by increasing average ticket sizes, lower interchange fees as a percentage of ticket size in 2027–2028 as transaction volume surpasses $5B, reduced third-party processing fees as a % of transaction fees as CTLP scales and improves transaction routing, and operating leverage from fixed costs. Rising ticket size contributes 80–85% to margin expansion, while cost efficiencies account for 15–20% by FY28. The table below illustrates transaction margin drivers based on a single average ticket size transaction:

Management expects subscription gross margins to remain in the 88–90% range. As of Q1’25, deployment and activation timelines have normalized to six weeks, suggesting backlog easing and a reacceleration of subscription revenue growth to 15%+ from 10.2% in FY24. The 95% retention rate of SEED customers, incremental software add-on revenue, and adoption of the Cantaloupe ONE program (bundling equipment and software) should sustain subscription margins, with my base case assuming annual 5bps improvements.

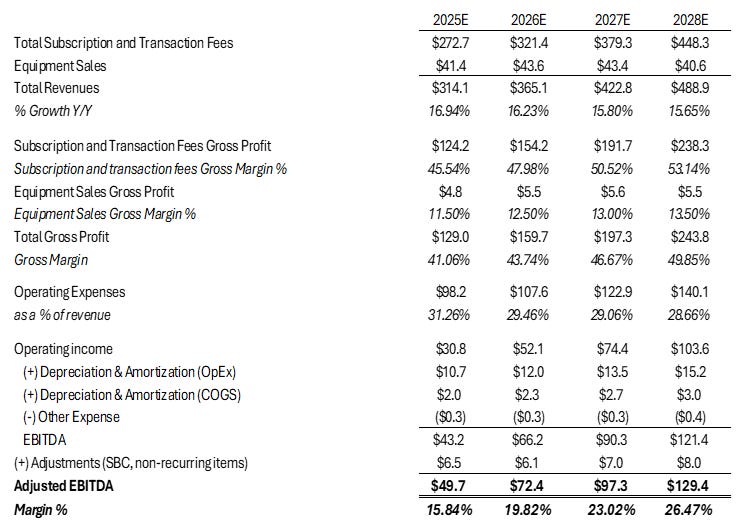

Transaction and subscription margins remain core EBITDA drivers. Additionally, my base case estimates equipment gross margins will reach 13.5% by FY28, at the midpoint of management’s 12–15% target. Management has also taken a disciplined approach to OpEx, expecting it to remain stable or slightly decrease from Q1’25 levels through FY25. I project Adj. EBITDA of $49.7M in FY25 (15.8% margin), slightly above management’s $48M midpoint guidance, and $72.4M in FY26 (19.8% margin), implying a 65% CAGR from FY22–FY26. All of the base case Revenue and Cost assumptions driving EBITDA are summarized in the table below:

Consensus estimates underestimate CTLP’s profitability trajectory, projecting only $46M in 2025 EBITDA and $60M in 2026. At my base case, CTLP trades at 12.19x EV/FY25E EBITDA and 8.38x EV/FY26E EBITDA, despite a 15%+ revenue CAGR, high recurring revenue, and strong operating leverage. These multiples, along with its current 17.3x EV/LTM EBITDA, are considerably low relative to the transaction/software peers’ median at 21.2x EV/LTM EBITDA. However, since many peers—including direct competitor Nayax—have only recently turned profitable, multiple expansion seems unlikely, and I expect share price appreciation to come from EBITDA growth.

Nayax, in particular, has been growing revenue at a faster rate than CTLP, driven by its presence in attended retail compared to CTLP’s exclusive focus on unattended retail/self-checkout. Additionally, Nayax benefits from a significantly larger international footprint (50%+ of revenue), a faster-growing software business, and an aggressive sales strategy (SG&A/Rev of 32% vs. CTLP’s 22%), which has delayed profitability, with Nayax only turning GAAP profitable in Q3’24.

In summary, CTLP outperforming EBITDA consensus estimates for next three quarters of FY25 should re-rate its EV/2025E EBITDA multiple to its current EV/LTM EBITDA multiple of 17.3x. Assuming no multiple expansion, this implies a 2025 price target of $11.72, representing ~44% upside from current levels.

Risks:

Downward Revision to FY25 Revenue Guidance:

In Q1’25 earnings, management reaffirmed FY25 revenue guidance, projecting:

· Total revenue: $308M–$322M

· Subscription & transaction fees growth: 15–20% Y/Y

· Net income attributable to common shares: $22M–$32M

· Adjusted EBITDA: $44M–$52M

· Operating cash flow: $24M–$32M

At the midpoint, management expects $315M in total revenue, driven by 17.5% Y/Y growth in subscription and transaction fees ($272M). This implies a significant step-up in equipment sales to $42.3M (+15.9% Y/Y), reflecting an expected rebound as the impact of the FY24 3G-to-4G upgrade cycle fades. However, in Q1’25, equipment sales declined -6.7% Y/Y to $7M, and another decline in Q2’25 would likely prompt a downward revision to total FY25 revenue.

While a revenue guidance cut would be a headline risk, the impact on profitability could be positive. If my base case for +17.8% Y/Y growth in subscription & transaction fees holds—slightly above the midpoint guidance—and equipment sales remain flat Y/Y instead of growing 11.50% (base case), Adjusted EBITDA would actually come in higher at $50.3M. This is due to the significantly lower projected 11.5% gross margin on equipment sales compared to the 45.5% gross margin on subscription & transaction fees, meaning weaker equipment sales would reduce revenue but improve overall profitability.

Summary Base/Bull/Bear Cases:

Disclaimer: Nothing posted by P14 Capital should be considered financial advice. Please consult a financial advisor and/or conduct your own due diligence before making investment decisions.

Good call here, pretty much hit your target right after the post. Do you think they’ll ultimately sell/go private at the end of their strategic review?

Thought this was really well done, and one of my favorite ideas I’ve read recently. Keep it up and feel free to DM me on X: komodo_capital.