$BBW - Build-A-Bear Workshop

Bottom Fishing for ~2x Upside

Disclaimer: Nothing posted by P14 Capital should be considered financial advice. The author of this post holds a long position in the stock discussed. Please consult a financial advisor and/or conduct your own due diligence before making investment decisions.

Build-A-Bear Workshop, Inc.

NYSE: BBW | 07/07/2026

Thesis Summary

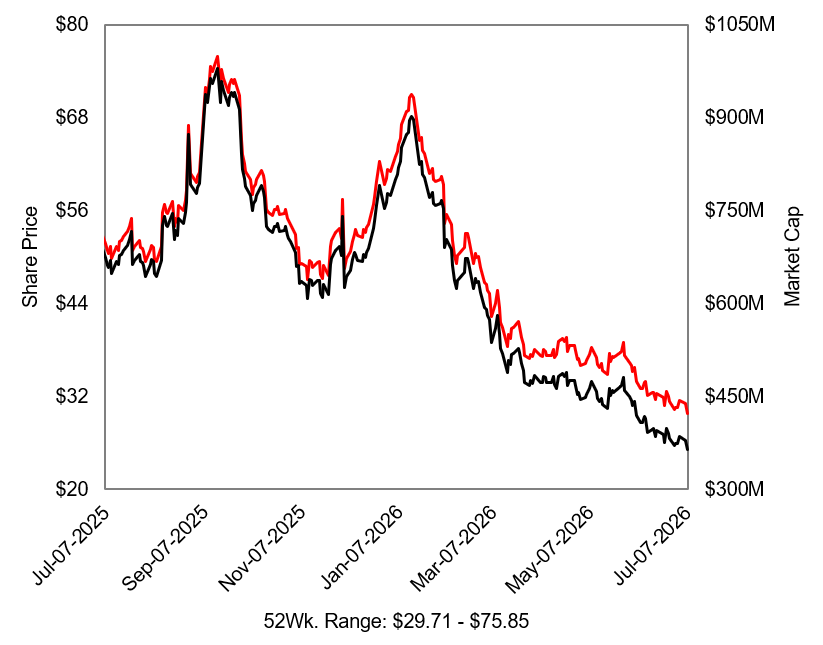

Mr. Market prices BBW as a post-COVID mall retail beneficiary whose earnings have peaked, with DTC sales and e-commerce traffic expected to enter terminal decline. Shorts have been rewarded immensely this year with shares down more than 50% YTD. The selloff has followed a barrage of negatives: weaker sentiment toward specialty retail, revenue misses, the retirement of longtime CEO Sharon Price John, 1Q27 marking the first revenue decline in eight quarters and first negative traffic quarter in seven, and a cut to FY27 revenue guidance. FY26 tariff costs and AI-driven search changes added further pressure on margins, online demand, and planned store visits. BBW’s TTM P/E has compressed by more than 50% since the start of the year, its EBITDA multiple is near a two-year low, and short interest is near a record 25% of float.

I think 1H27 marks the operational bottom, with several dynamics supporting a recovery in 2H27. The first catalyst for shares is a low bar into the 2Q27 print. Management’s commentary came only 3.5 weeks into the quarter and extrapolated weak 1Q27 traffic and digital trends through the remainder of Q2, leading consensus to expect another revenue decline, with 2Q27 projected to be worse than 1Q27. Since then, BBW has had a full quarter of its new Hello Kitty stores, the Toy Story 5 launch, strong graduation demand, NBA and World Cup-related sales, and new promotional activity. Alternative data points to a Q1 bottom and improving traffic from late May onward. With short interest near 25% of float, even a modest beat or improved 2H27 commentary could trigger a short squeeze.

Beyond the near-term print, social arbitrage between customer demand and the stock price continues to widen. Wearable plush, bag charms, Sanrio, and Pokémon releases are gaining traction with teens and adult collectors, while BBW posted its best Valentine’s Day in North American history, a solid Easter, and continues to sell more than 20K Birthday Treat Bears per week. The 2H27 calendar also improves with the world’s largest Build-A-Bear store opening at ICON Park, the company’s 30th anniversary, a refreshed Harry Potter collection, Halloween, and Black Friday. The licensed slate stays strong into FY28 with Shrek 5, Spider-Man: Beyond the Spider-Verse, Bluey, and Avengers: Secret Wars. BBW has relationships with the studios behind these franchises, giving the company several opportunities to launch licensed products around major releases. The stock price gives little credit to the customer response or improving product and event pipeline.

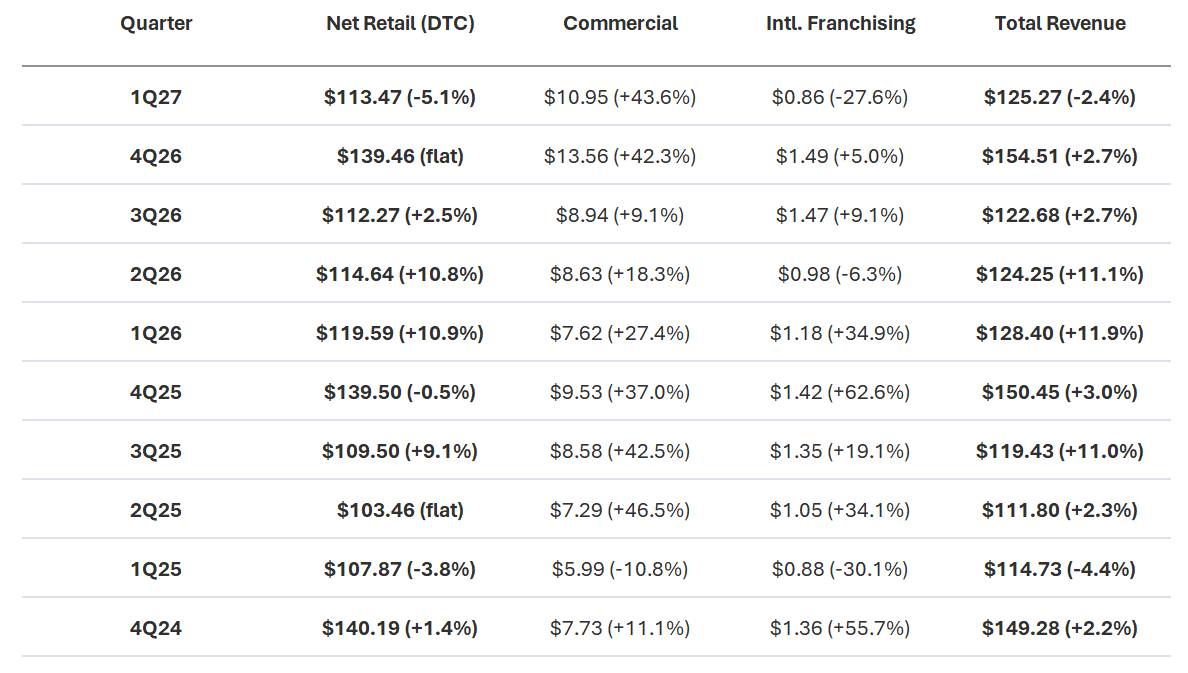

Mr. Market is also giving little credit to the mix shift in the business. Commercial revenue has grown at a 54% CAGR since 2020 and increased another 43.6% Y/Y in 1Q27 as BBW expands through partner-operated locations and wholesale distribution. Partner locations generate a 106% ROIC versus 21% for traditional retail, while Commercial carries a 53.1% pre-tax margin versus 9.2% for DTC. International Franchising adds another capital-light growth avenue, with a 26.4% pre-tax margin, 49% ROIC, and room to grow from 112 locations toward management’s long-term target of 300. More than 40% of the global footprint is already outside traditional malls, and the Walmart rollout has shown that BBW products can sell well outside the workshop environment.

The $13.2M tariff refund supports FY27 earnings, while higher average transaction values, lower merchandise costs, Commercial scale, IP licensing, and International Franchising should support margins over time. BBW has zero debt, stable capex, and no appetite for acquisitions, leaving a large portion of FCF available for buybacks. The company has already reduced shares outstanding by more than 25% from its 2019 baseline and has accelerated repurchases during the recent selloff.

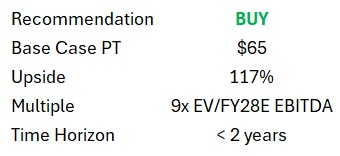

Under my base case, revenue grows at a 4.1% CAGR through FY29, pre-tax margin expands 83 bps, and diluted EPS compounds at 10.3%. Applying 9x FY28 EBITDA gives me a price target of ~$65/share, or +117% from current levels, versus ~20% downside to ~$24/share in my bear case. A 2Q27 beat and improved outlook could pull the upside forward considerably given the current short interest and depressed multiple.

Business Overview

Build-A-Bear Workshop, Inc. (BBW) is a global experiential toy retailer built around the in-store creation and customization of stuffed animals. Founded in 1997, the brand has expanded beyond its traditional mall base into tourist destinations, partner-operated venues, international franchises, and digital channels. As of May 2, 2026, BBW had 669 locations across 37 countries, including 376 company-operated stores, 181 partner-operated locations, and 112 international franchise locations. The company hosts 50M+ guests each year, with North America accounting for 92% of revenue.

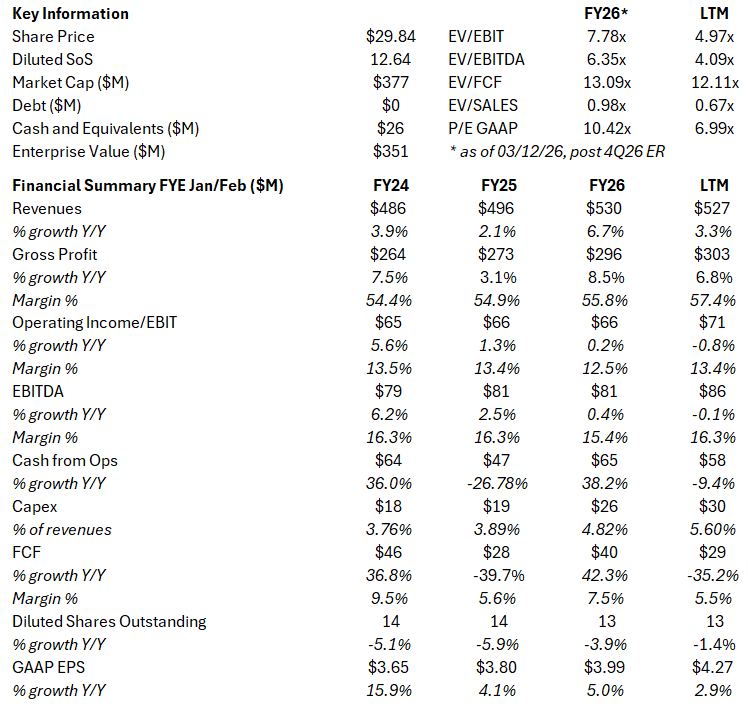

In FY26 (ended January 31, 2026), BBW generated record revenue of $529.8M, up 6.7% Y/Y and 13.2% from FY23, while pre-tax income reached $67.3M. Pre-tax margin was 12.7%, down 84 bps Y/Y, primarily due to ~$11M of tariff-related costs.

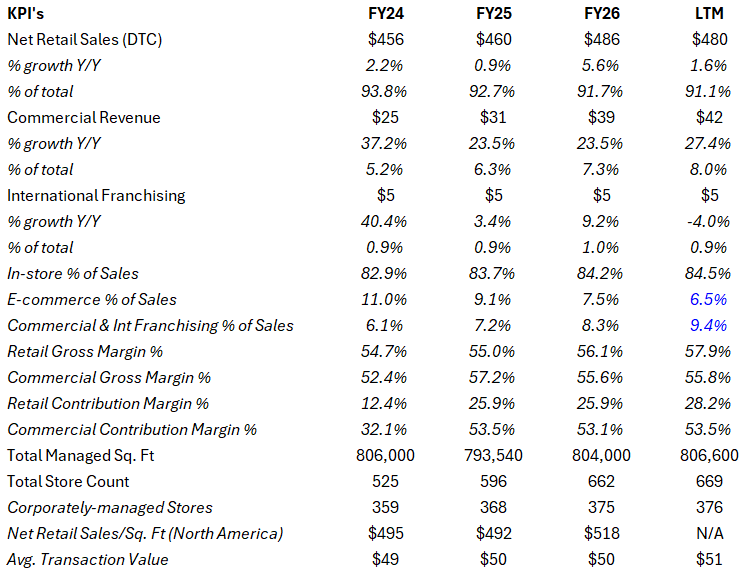

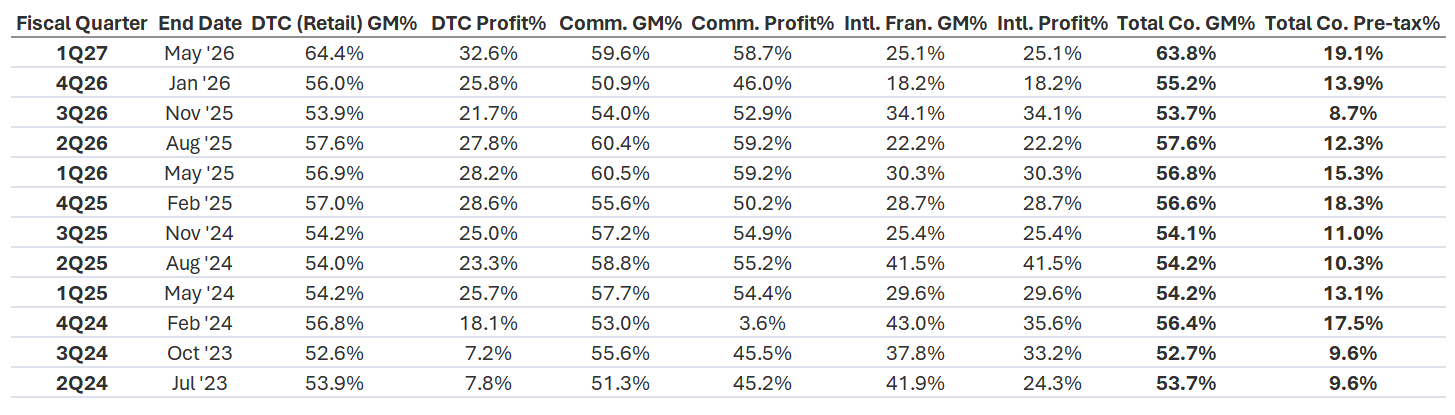

The company operates across three segments. Direct-to-Consumer, its largest segment, generated ~$486M of revenue and $121.6M of contribution margin, with 80% of sales coming from company-operated stores and 20% from e-commerce. Commercial generated $38.7M of revenue, up 23.5% Y/Y, and $9.2M of contribution margin through wholesale product sales and IP licensing. International Franchising generated $5.1M of revenue and $1.7M of contribution margin from royalties, development fees, and product sales to master franchise partners.

BBW’s core model monetizes each stage of the customer experience. Guests select a plush toy for $14-$40, participate in the stuffing and Heart Ceremony, then add clothing, footwear, sounds, scents, and accessories for $7-$25. The model drives high-intent traffic, with 80% of store visits planned in advance. Online customers can replicate parts of the experience through the 3D Bear Builder or purchase pre-built licensed products and collectibles.

The customer base has expanded well beyond families with young children. Teens and adults now account for ~40% of revenue, supported by pop-culture and sports licenses, collectibles, gifting, and the age-gated Bear Cave assortment. The product mix combines licenses from partners such as Disney, Nintendo, and Warner Bros. with owned IP, including Glisten and Merry Mission, which has generated more than $150M since launch.

The company executes its sales model through a four-pillar strategy: Organic Growth, Location Expansion, Wholesale/Outbound Licensing, and Gifting/Personalization. The operation relies on ~5,500 employees across 37 countries.

BBW participates across the $108B global toy market, the multi-billion-dollar personalization and gifting market, and the ~$15B global plush market, which is expected to grow at a MSD CAGR through 2033. The company competes with mass-market toy manufacturers such as Mattel and Hasbro, legacy brands such as Ty, and newer plush competitors including Squishmallows and Jellycat.

BBW differentiates itself through the experience attached to the product. Customers create and customize the product themselves, with the Heart Ceremony adding an emotional component that is difficult to replicate in a big-box aisle or through a standard online transaction. The model has helped BBW build a database of 20M+ first-party contacts while supporting gross margins near 54% and ROE near 35%.

The company has also broadened its footprint through smaller store formats, tourist destinations, shop-in-shops, and partner-operated locations. Since January 2024, BBW has added 135 net locations to reach 669 global sites, giving the company more ways to expand beyond its traditional mall base.

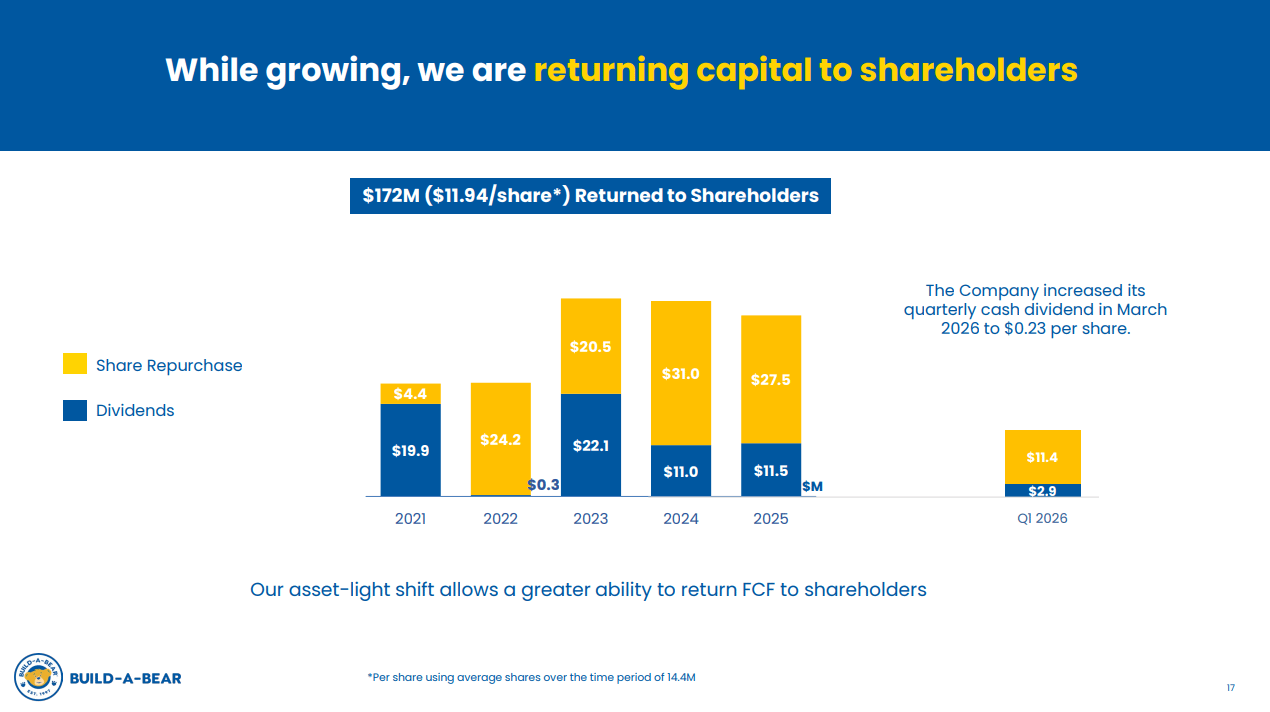

BBW has zero debt and $26M of cash. Since 2021, the company has returned more than $180M to shareholders through buybacks and dividends and has reduced shares outstanding by more than 25% from the 2019 pre-pandemic baseline. The quarterly dividend was increased for the third consecutive year in March 2026 to $0.23 per share, equal to a ~3% yield.

CEO Chris Hurt assumed the role on June 11, 2026, after serving as Chief Operations and Experience Officer since 2015. CFO Voin Todorovic joined BBW in 2014 after previously leading finance for Wolverine Worldwide’s Lifestyle Group. Executive compensation is heavily performance-based, with annual incentives tied to revenue and EBITDA margin and most of the CEO’s long-term compensation tied to multi-year operating targets.

FY27: A Tale of Two Halves

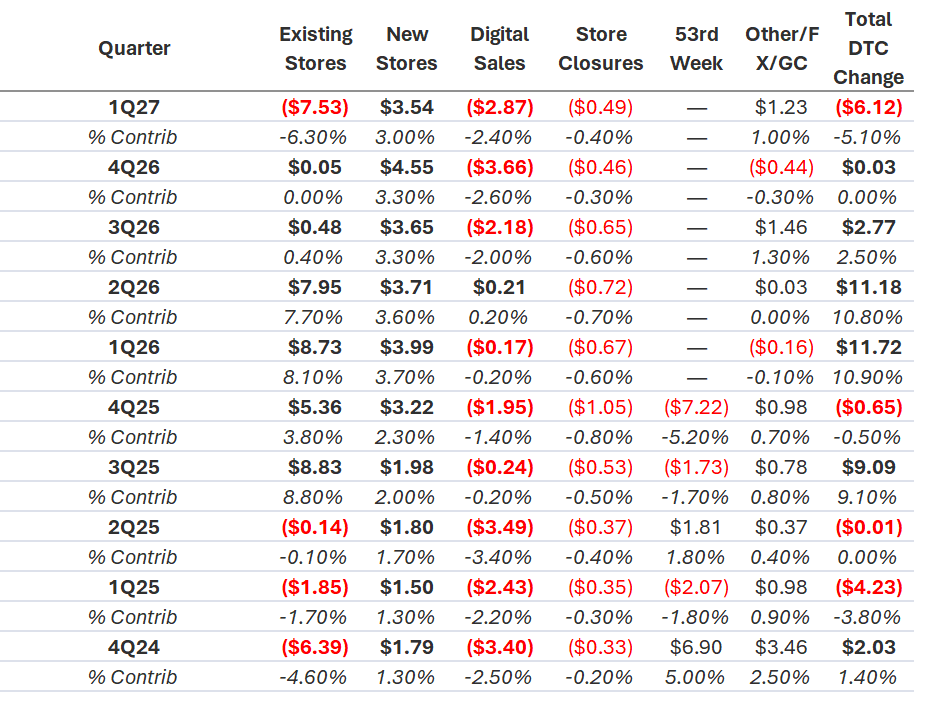

In my view, 1H27 represents the operational bottom. BBW’s YTD weakness has been driven by a sharp slowdown in revenue growth and traffic, with the stock reacting exactly as you would expect in a world dominated by pod bros making L/S decisions based on re-acceleration or deceleration in the P&L. For BBW, the latter was particularly evident in 1Q27.

1Q26 was one of the strongest quarters in the company’s history. Revenue grew 11.9% Y/Y, including an $8.7M increase from existing DTC stores alone, as store traffic significantly outperformed national retail trends. The company leaned into an offensive market-share strategy backed by the success of licensed collections such as Hello Kitty and Pokémon, while the launch of Mini Beans added a new high-volume category at a ~$10 entry price that quickly gained traction with both children and adult collectors.

1Q27 was forced to lap that strength with a weaker product lineup and fewer major launches. Retail traffic fell 7% Y/Y, with adverse winter weather costing an estimated $2M of revenue, while e-commerce demand dropped 26% as AI-driven search changes pressured organic traffic. The digital weakness also affected stores, as 80% of visits are planned in advance and the website often serves as a research tool before customers visit a workshop. Combined with weaker consumer sentiment and lower mall traffic, existing-store sales, typically the largest driver of revenue growth, came under significant pressure.

1H26 was a period of unpressured growth, creating the toughest comparisons of FY27 in the first half. The market is treating the 1Q27 slowdown as the start of prolonged weakness, whereas I think FY27 is more likely to be a tale of two halves as comparisons ease and the product and event calendar improves.

Upside to the 2Q27 Print

BBW’s P/E multiple has compressed by more than 50% since the start of the year, with significant pessimism already embedded ahead of the 2Q27 print on 08/27.

Much of that pessimism stems from management’s tone on the 1Q27 call. BBW does not provide quarterly guidance, but in 4Q26 management initially guided for 4-6% FY27 revenue growth, -3% to +3% pre-tax income growth, at least 20% Commercial growth, and 50+ net new locations. After 1Q27 marked the company’s first revenue decline in eight quarters and first negative traffic quarter in seven, management cut FY27 revenue guidance to 0-3.8% growth.

The bottom-line outlook moved in the opposite direction as pre-tax income guidance was raised to +7.1% to +16.1% Y/Y due to stronger margins and the $13.2M IEEPA tariff refund, with $7M recognized in 1Q27 and another ~$6M expected to flow through inventory later this year. The revenue guide was reset lower after management extrapolated weak 1Q27 trends and the first 3.5 weeks of 2Q27 through the remainder of the quarter, while still expecting a recovery in 2H27.

Management also said 2Q27 revenue would decline Y/Y and likely perform worse than the 2.4% decline in 1Q27. Consensus agrees, expecting revenue to fall 2.6% Y/Y as BBW laps 11.1% growth in 2Q26, while a fourth consecutive revenue miss would surprise few investors.

I think the bar is low enough for an upside surprise. The guidance reset came early in the quarter, after only 3.5 weeks, and the next print will be the first under a new CEO who had every incentive to avoid overpromising in the 1Q27 call. Several product, seasonal, and traffic indicators also suggest the quarter could finish better than management’s early commentary implied.

The first full quarter of the new Hello Kitty and Friends themed stores at Mall of America and American Dream should provide incremental revenue, particularly given how important Hello Kitty was to 1Q26 growth.

Toy Story 5, released on June 19, gives BBW another major licensed product catalyst. The collection spans premium products priced at $60-$70 and higher-volume Mini Beans at $12.50, giving the company exposure across multiple price points.

Graduation merchandise also appears to have performed well in June, with reports of early sellouts in several regions. Sports could provide another smaller source of upside. BBW has a broad NBA licensing relationship, while country-themed bears and apparel have reportedly seen strong demand around the World Cup despite the company not holding rights to official tournament collectibles. Neither the NBA Finals nor the World Cup received meaningful attention on the 1Q27 call. The recently launched Summer of Mystery promotions could also help engagement.

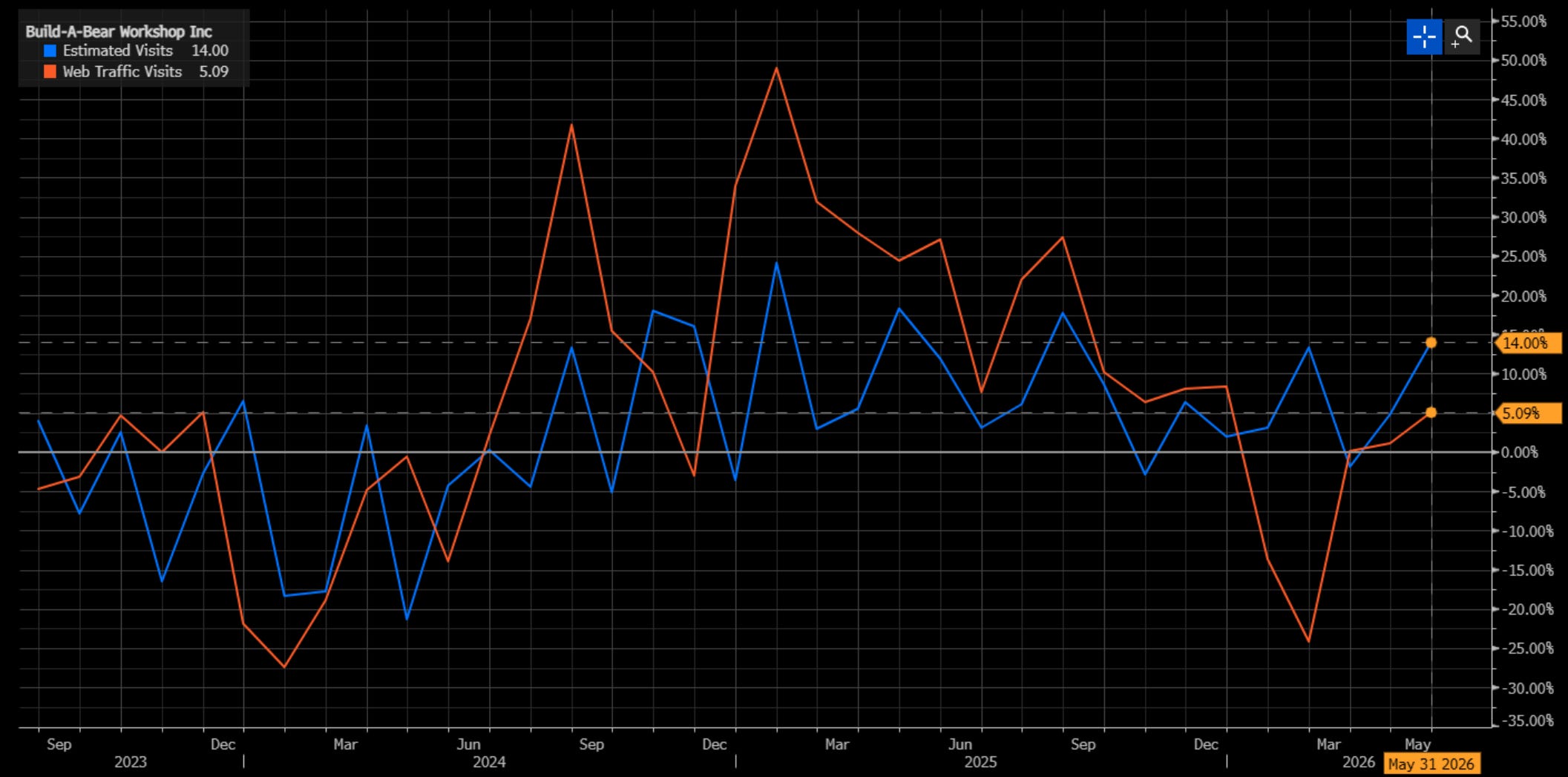

The more speculative evidence comes from alternative data. Placer.ai store traffic and Similarweb web traffic both point to a 1Q bottom and improvement beginning in late May. I would not rely on either dataset in isolation, especially for a small-cap company, but the direction is encouraging and runs against the straight-line weakness implied by management’s early-quarter commentary.

Taken together, the bar for 2Q27 looks low relative to the number of potential upside drivers that developed after the 1Q27 call. With the multiple near a two-year low and short interest near a record ~25% of float, even a modest beat or improved 2H27 commentary could trigger a meaningful squeeze.

Social Arbitrage and an Improving Content Slate

Even if 2Q27 comes in weak, the setup for a stronger 2H27 is intact. The social arbitrage lies in the gap between what is gaining traction with customers and the prolonged weakness being priced into the stock.

In May 2026, BBW launched Slushie Plushies, its first wearable plush, as customers increasingly “style and show off” their products. The same trend has extended into $20 bag charms, which management says are “on fire” across stores and are attracting teens and adult collectors. This is part of a broader shift in the toy market, where adults are becoming a larger source of demand. The U.S. toy market grew 13% Y/Y in early 2026, with consumers aged 18+ driving 35% of the growth.

Seasonal demand also held up better than the 1Q27 headline suggests. BBW had its best Valentine’s Day in North American history and a solid Easter, while the Birthday Treat Bear program continues to sell more than 20K units per week. These results are difficult to square with the market treating BBW as a brand entering prolonged decline.

Collector demand provides another source of repeat traffic. The Pokémon Eevee Evolution series includes eight limited-time releases throughout the year, while the Sanrio Ice Cream Shop collection is performing well with the kidult demographic. Limited releases, owned IP, and licensed collections give BBW more ways to drive repeat purchases beyond the traditional family visit.

While 1H27 laps the toughest comparisons in company history, the 2H27 product and event calendar is much stronger. Late summer brings the opening of the world’s largest Build-A-Bear store at ICON Park Orlando, giving the company a new destination location in one of the country’s largest tourist markets with opportunities across retail, events, and tourism traffic.

October marks BBW’s 30th anniversary, giving the company an obvious nostalgia campaign aimed at adults who grew up with the brand and now bring their own children. A refreshed Harry Potter collection is also timed around the new HBO series, while Halloween and Black Friday add two of the brand’s most important seasonal periods.

The licensed slate stays strong into FY28, with Shrek 5, Spider-Man: Beyond the Spider-Verse, Bluey, and Avengers: Secret Wars all scheduled for 2027. BBW has relationships with the studios behind these franchises, giving the company several opportunities to launch licensed products around major releases.

The Capital-Light Strategy and the Mix Shift

BBW is expanding beyond traditional workshops through partner-operated locations and wholesale distribution in venues such as Walmart, Carnival Cruise Line, Great Wolf Lodge, and SeaWorld. In the partner-operated model, the partner bears the cost of store build-outs, real estate, labor, and inventory, which is purchased from BBW on a wholesale basis. Partner locations generate a 106% ROIC versus 21% for traditional retail, allowing BBW to expand faster with little capital at risk.

Commercial revenue has grown at a 54% CAGR since 2020 and increased another 43.6% Y/Y in 1Q27, making it the strongest part of the business even as DTC weakened. The opportunity has also expanded beyond experience-based locations into traditional wholesale, led by the launch of Mini Beans across 1,500 Walmart stores.

The strategy gives BBW another source of growth while reducing its dependence on mall traffic. More than 40% of the global footprint is now outside traditional malls, and partner-operated locations have more than doubled since mid-2023. Wholesale also increases brand awareness and product trial among customers who may later visit a workshop.

The Walmart rollout could open the door to additional large retail partnerships (TGT, etc.) Even without another Walmart-sized deal, management expects Commercial revenue to grow at least 20% for the fifth consecutive year in FY27 and is investing in the infrastructure needed to support a much larger global distribution network.

The mix shift is also highly accretive. Commercial carries a 53.1% pre-tax margin because partners absorb most operating costs, while BBW earns revenue through wholesale product sales and high-margin IP licensing. Commercial and other third-party channels now account for 32% of LTM pre-tax income, up from a loss in 2019.

BBW is also using more flexible store formats to improve returns on new locations. Traditional Discovery stores generate higher margins but require more upfront capital, while smaller Concourse and shop-in-shop formats produce lower margins with significantly higher cash-on-cash returns. The broader range of formats gives BBW more options to enter high-traffic locations without relying on the economics of a full-size mall store.

The market is giving little credit to the margin benefit from this shift. Even through the FY26 tariff pressure, selective price increases and a growing Commercial mix helped protect profitability relative to pre-tariff levels. As Commercial becomes a larger share of revenue and pre-tax income, BBW should be able to grow earnings faster than revenue. 1Q27 margins should not be used as the baseline, however, because they were inflated by the partial tariff refund.

Going Global

International Franchising is the second leg of BBW’s capital-light strategy. Outside the company-operated markets of the U.S., Canada, U.K., and Ireland, management sees room to grow from 112 franchise locations today to as many as 300 over time. The brand has already expanded from 19 countries to 37 in just two years, with recent entries into Germany, Norway, Italy, and the Philippines.

International Franchising carries a 26.4% pre-tax margin versus 9.2% for DTC and generates a 49% ROIC, giving BBW another way to expand with limited capital. Many of these markets are also much earlier in the brand’s development and have less direct competition in experiential toy retail.

International markets have another advantage in the current environment. Product can generally be sourced directly from China without the same U.S. tariff burden, reducing some of the volatility affecting the domestic business.

BBW is also giving franchisees access to the smaller formats developed for its corporate fleet, including Concourse and shop-in-shop locations. These formats lower the upfront investment required to enter new markets and make it easier to secure high-traffic locations where a full-size Discovery store may not make economic sense.

With the current franchise base still well below management’s long-term target, International Franchising provides a long runway for high-margin, capital-light growth alongside Commercial.

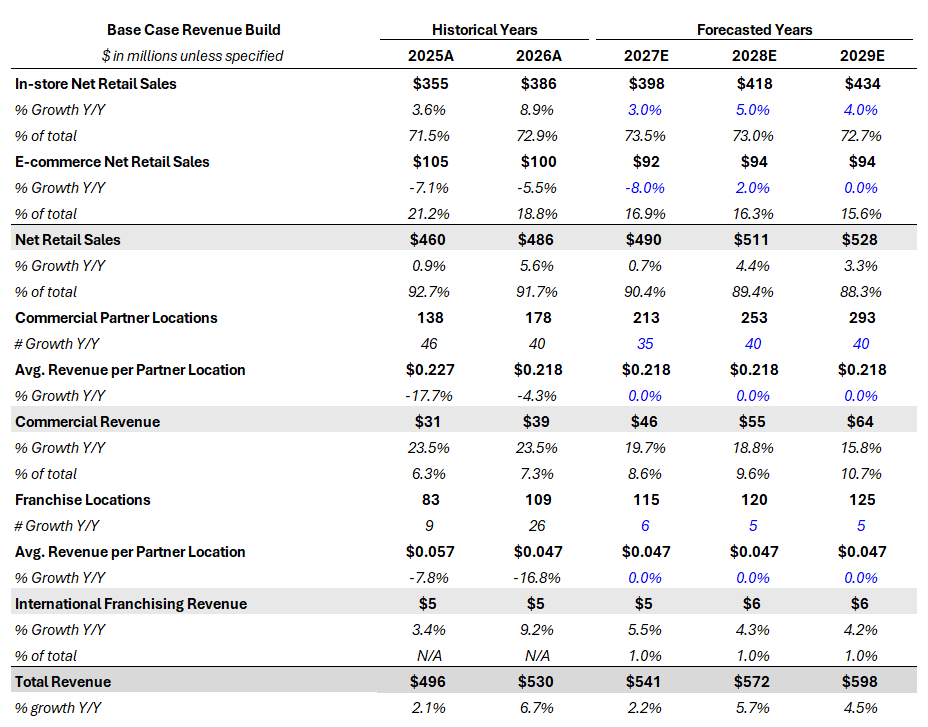

Revenue, Margin, and FCF Build

I project FY27 revenue growth of 2.2%, slightly above management’s 1.9% midpoint, driven by a recovery in 2H27. E-commerce should remain a drag this year, but I expect declines to reverse in FY28 as management adjusts to changes in search and improves its digital strategy, followed by flat sales in FY29. In-store sales should recover in 2H27 and accelerate in FY28 as comparisons ease, the content slate improves, and new high-traffic locations such as ICON Park ramp. Overall, I project Net Retail Sales to grow at a 2.8% CAGR through FY29.

Commercial should continue to lead growth. The model is highly scalable, and the Walmart rollout increases the likelihood of further wholesale wins. I project an 18% Commercial revenue CAGR through FY29, driven primarily by distribution and location growth while holding ARPU flat. International Franchising should grow faster than the overall business but slower than Commercial, where I expect management to focus more heavily given the larger opportunity and stronger economics.

In my base case, total revenue grows 2.2% in FY27, 5.7% in FY28, and 4.5% in FY29, or a 4.1% CAGR. I view MSD long-term growth as reasonable given BBW’s repeat-purchase behavior, expanding distribution, and ability to drive demand through new products and seasonal events.

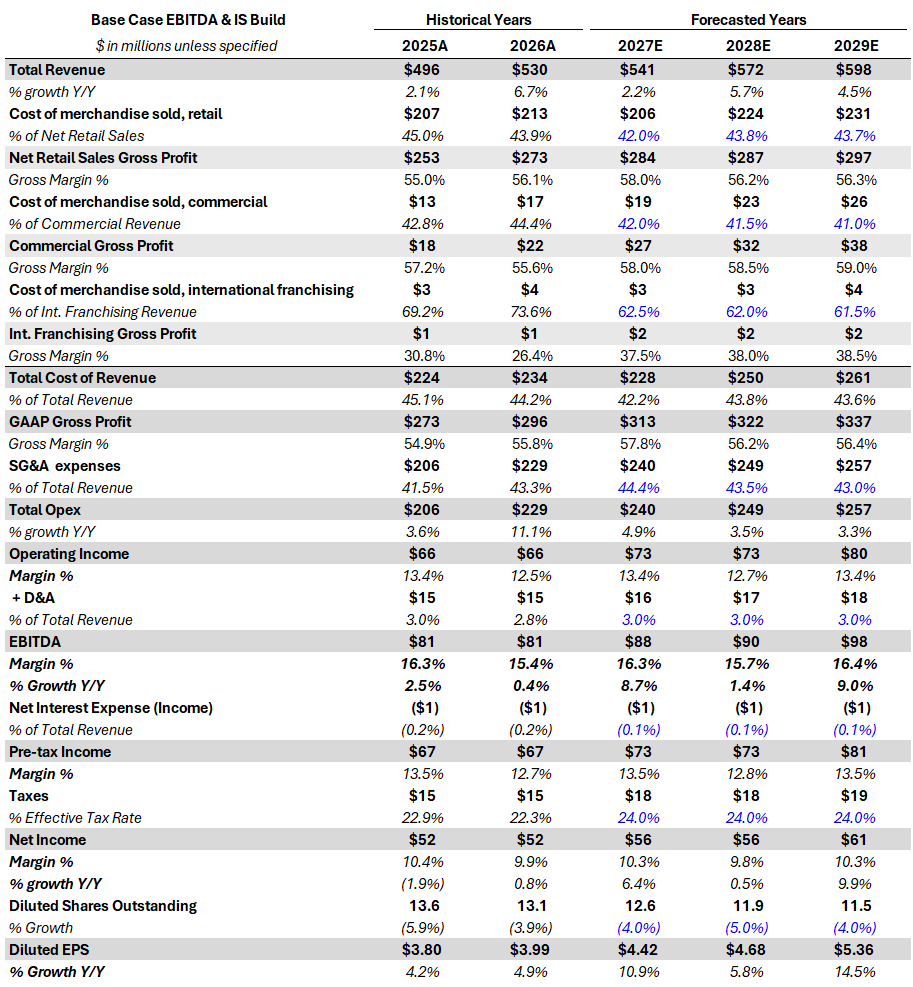

FY27 margins benefit materially from the $13.2M tariff refund. I estimate Net Retail Sales gross margin expands ~190 bps Y/Y, with most of the increase tied to the refund. Gross margin should normalize in FY28 but stay above FY26 levels as higher average transaction values and lower merchandise costs offset the loss of the one-time benefit.

I expect Commercial gross margin to expand ~200 bps in FY27 and continue improving at a slower pace as IP licensing becomes a larger part of the mix and the business scales across more distribution points with limited incremental cost. International Franchising should also benefit from lower tariff exposure and similar scale economics. Across the business, I forecast 62 bps of gross margin expansion through FY29.

SG&A should stay elevated in FY27 due to 1H27 operating deleverage, continued digital investment, and higher compensation costs. I expect SG&A growth to slow in FY28 and FY29 as revenue reaccelerates, resulting in 83 bps of pre-tax margin expansion over the forecast period.

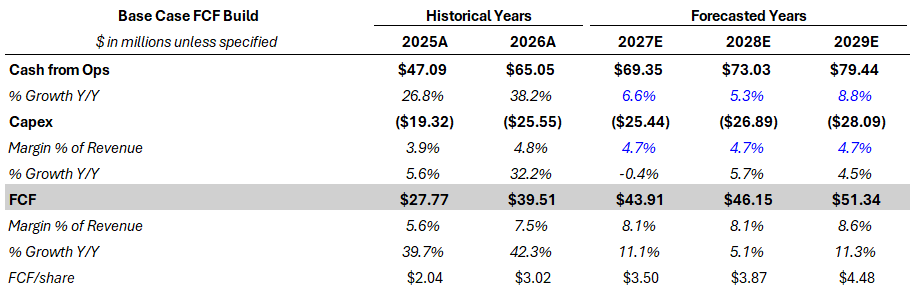

Higher earnings and stable capital intensity should translate into more FCF available for buybacks. BBW is not an acquisitive business, and I hold capex at 4.7% of revenue. The company repurchased 509K shares in FY26 and another 338K through late May, equal to ~2.6% of the share base in less than four months, with the pace accelerating as the stock sold off.

I forecast diluted share count declines of 4% in FY27, 5% in FY28, and 4% in FY29. The buybacks should be especially accretive in FY28, when pre-tax income laps the tariff refund, helping diluted EPS compound at a 10.3% CAGR through FY29.

Valuation and Risks

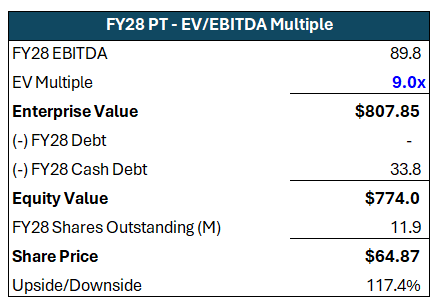

Under my base case, I value BBW at 9x FY28 EBITDA, implying a price target of ~$65/share, or +117% from current levels, to be achieved in under two years. The stock could reach that level sooner if a 2Q27 beat and raise forces shorts to cover.

BBW currently trades near its lowest EBITDA multiple in more than two years. Under my base case, I expect the multiple to recover toward, but remain below, the prior peak of ~11x. The name of the game is to buy low and sell high.

E-commerce is the most immediate risk. Management has only recently begun adjusting its digital strategy through a mobile-first approach and changes to SEO. Continued weakness in organic traffic could weigh on both online sales and store visits. I would also like to see BBW become more aggressive on platforms such as TikTok, where toy discovery and social shopping continue to gain share.

Weaker consumer sentiment, lower discretionary spending, and softer mall traffic could delay the 2H27 recovery and pressure the multiple.

Tariffs could return as a headwind. A full reinstatement would pressure merchandise costs and reduce the margin upside in my forecast. The thesis also depends on execution around major seasonal periods and product launches, making a weak Halloween or holiday season another downside risk.

BBW also needs to protect the in-store experience. The workshop model is the company’s core competitive advantage, and pushing too far into standard wholesale at the expense of the experiential business could weaken the brand over time.

Under my bear case, I see ~20% downside to ~$24/share.

Conclusion

Build-A-Bear has established itself as the leader in experiential plush retail, with a durable brand, strong unit economics, and an increasingly capital-light growth model. Bears have extrapolated a difficult 1H27 compare into prolonged weakness while giving little credit to the improving 2H27 setup, Commercial growth, margin mix shift, or continued buybacks.

With BBW trading near its lowest multiple in more than two years, I view the risk/reward as attractive and I am long at ~$31/share.