$BDC - The Networking Stock to Rule Them All

90%+ upside in a mispriced IT/OT networking leader at an inflection

NOK, CSCO, EXTR and other networking stocks have had a face-ripping rally YTD. It should be obvious by now that networking and connectivity are solidifying their importance in the ongoing historic AI infrastructure buildout. How else are you going to token-maxx without said tokens reaching you? How is the next wave of Physical AI going to be powered without connectivity?

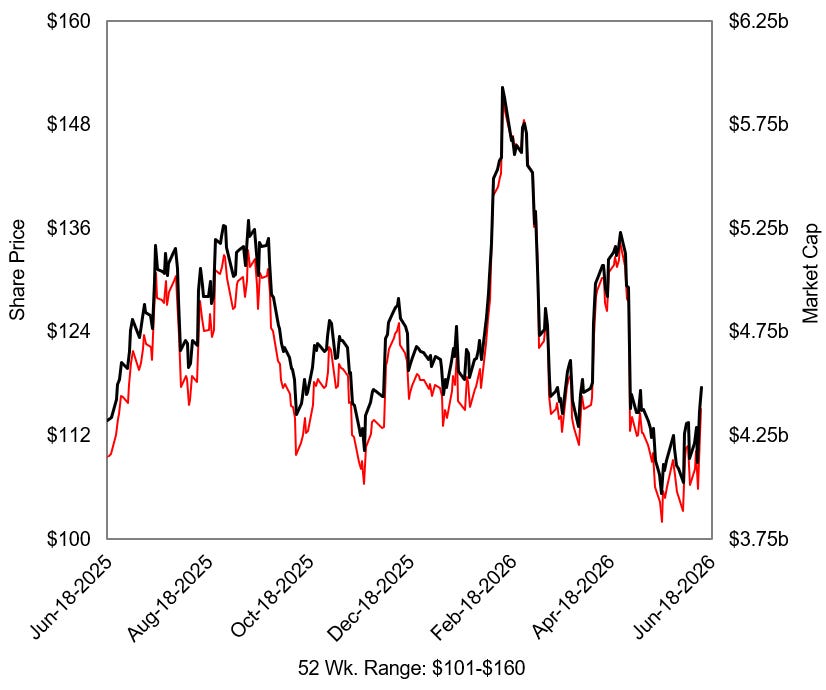

Among the sea of green in networking, there lies a stock that has not participated in the rally and now trades with unusually attractive risk/reward, a recovering chart, with the stock up ~15% since first alert, and an undemanding valuation.

Relative value is extremely important for single-stock theses going forward. In an environment where momentum stocks occasionally get violently dumped into the bin, the market quickly searches for value within growing sectors. The stock pitched today has this characteristic of relative value while also inflecting on growth and margins.

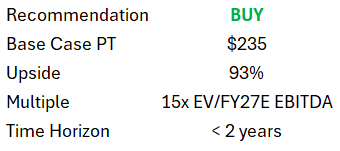

P14 sees ~90%+ upside potential in less than 2 years in this NETWORKING STOCK TO RULE THEM ALL.

Disclaimer: Nothing posted by P14 Capital should be considered financial advice. The author of this post holds a long position in BDC. Please consult a financial advisor and conduct your own due diligence before making investment decisions.

Happy Reading!

Belden Inc.

NYSE: BDC | 06/22/2026

Thesis Summary

Belden (BDC) is priced like a cyclical legacy cable company despite its shift into higher-value connectivity, active networking and IT/OT solutions. The business is repositioning across industrial automation, smart buildings and broadband, with a serviceable TAM that is due for rapid expansion. The market is still underwriting BDC as an LSD-MSD top-line grower even though the business is exiting the post-COVID destocking cycle with improving demand across all three core verticals.

The main overhang is the RUCKUS acquisition, which raises leverage near term and looks expensive at ~13x projected 2026 adjusted EBITDA versus BDC’s standalone multiple. In my view, the market is focused on the headline multiple and missing what the deal changes. RUCKUS adds a faster-growing, higher-margin active networking asset with 48K+ customers, 32% Y/Y revenue growth in 2025, 60%+ gross margins and 20%+ adjusted EBITDA margins in the first full year of ownership. It also gives Belden the active wireless and switching layer needed to sell a more complete network architecture from the industrial edge to the enterprise campus. The overhang is the opportunity because RUCKUS changes the growth, margin and strategic profile of the combined business.

The core business is also inflecting before giving credit to RUCKUS or the call options. Automation is shifting from destocking recovery to a longer upgrade cycle driven by reindustrialization, labor scarcity and higher automation intensity. Broadband is past the inventory correction and entering a multi-year upgrade cycle tied to higher speeds, fiber density and BEAD-funded deployments. Smart Buildings is no longer a CRE proxy, with demand shifting toward healthcare, hospitality, education, institutional retrofits and data center gray space. Across the business, Belden is moving from component sales toward solutions wins that combine passive infrastructure, active hardware, software, security and support.

The margin thesis follows suit with the mix shift. Traditional wire, cable and connector sales carry gross margins in the 36%-37% range, while full solutions can command gross margins in the 50% range. RUCKUS should push consolidated gross margins to ~40% post-close and help move solutions mix toward 30% of revenue by FY28. I model consolidated GAAP gross margins expanding 445 bps over the next 3 years and EBITDA margins expanding 473 bps, with most of the step-up arriving in 2027 as RUCKUS is fully integrated.

Consensus looks stale or overly conservative. FY26 consensus implies only LSD BDC-only growth if one quarter of RUCKUS contribution is included, while 2027 and 2028 estimates appear disconnected from the recovery and acquisition contribution. I model revenue inclusive of RUCKUS at $3.16B in FY26E, $4.1B in FY27E and $4.5B in FY28E, implying a 2026-2028 CAGR of +18.7%. Physical AI, edge computing and localized inference are additional upside paths because each requires secure, low-latency local networking infrastructure that Belden already sells.

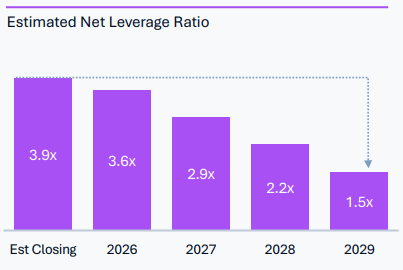

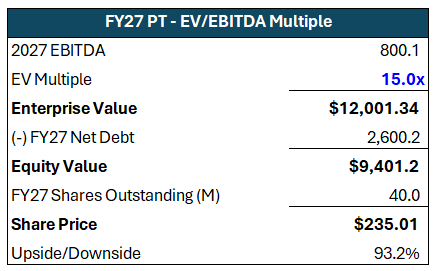

Even after accounting for the new leverage, P14’s FY26E EV/EBITDA estimate is ~14.5x versus the comp set mean of 21.4x. If the base case is executed, I think BDC can trade at 15x FY27E EBITDA within the next two years as revenue growth, margin expansion, RUCKUS synergies and consensus revisions take center stage. Using management’s 2.9x net leverage target by 2027 and a steady share count, my base case price target is $235/sh, or +93% from current levels. In a bear case, I see ~20% downside to $100/sh.

Business Overview

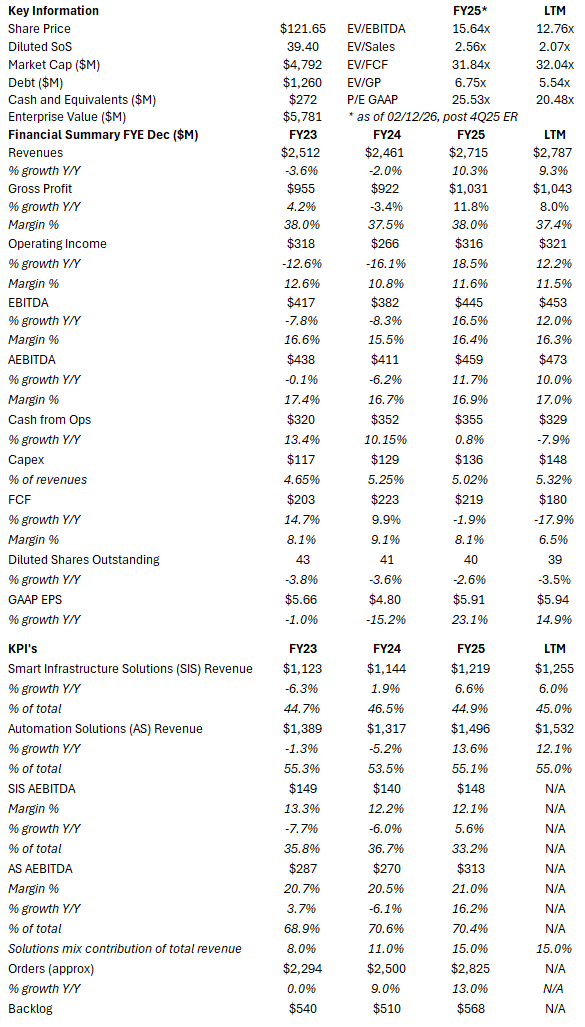

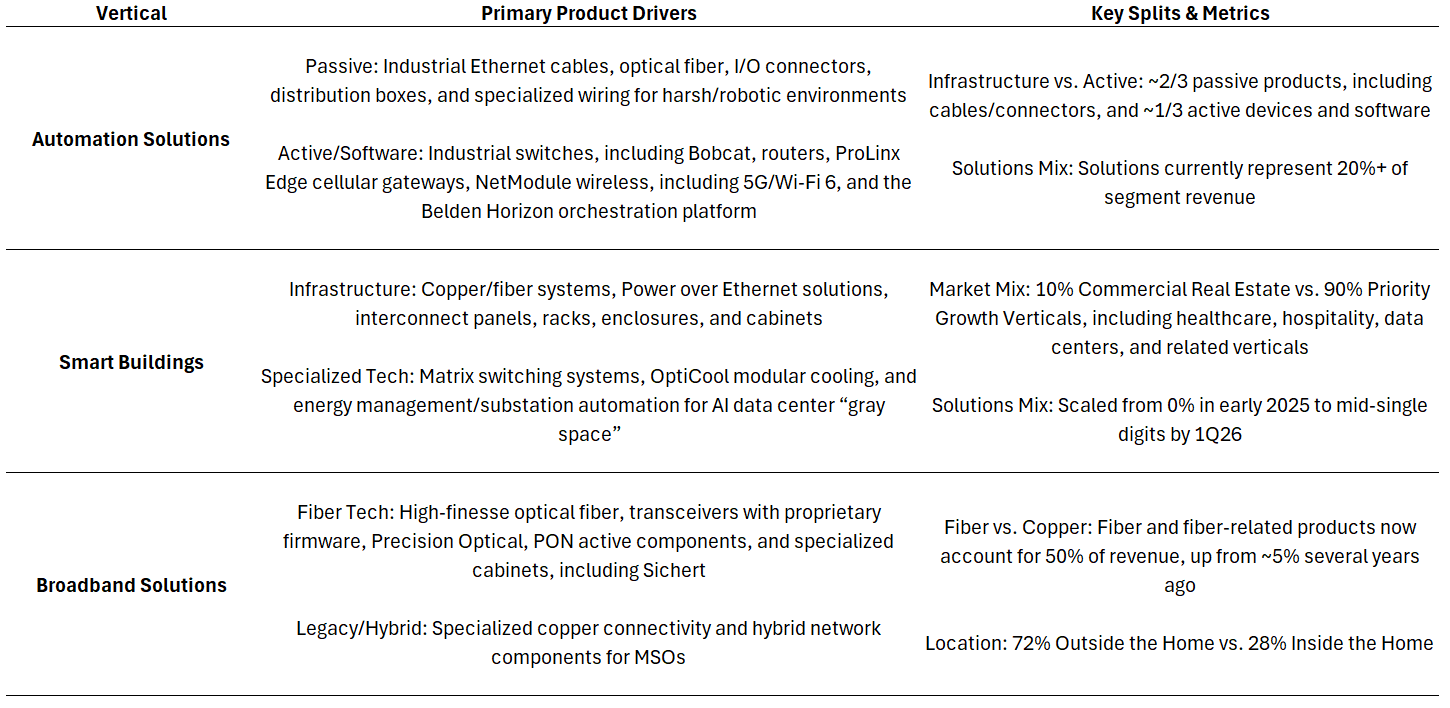

Belden Inc. (BDC) was founded by Joseph Belden in 1902 and later incorporated in Delaware in 1988. Today, the company serves more than 48,000 customers across industrial automation, smart buildings, broadband and other mission-critical end markets. Automation Solutions is the largest revenue driver at 55% of FY25 revenue, followed by Broadband at 23% and Smart Buildings at 22%. Belden previously reported through Enterprise Solutions, also referred to as Smart Infrastructure Solutions, which included Broadband and Smart Buildings, and Industrial Automation Solutions. Effective January 2026, the company reports as a single segment under a unified operating model.

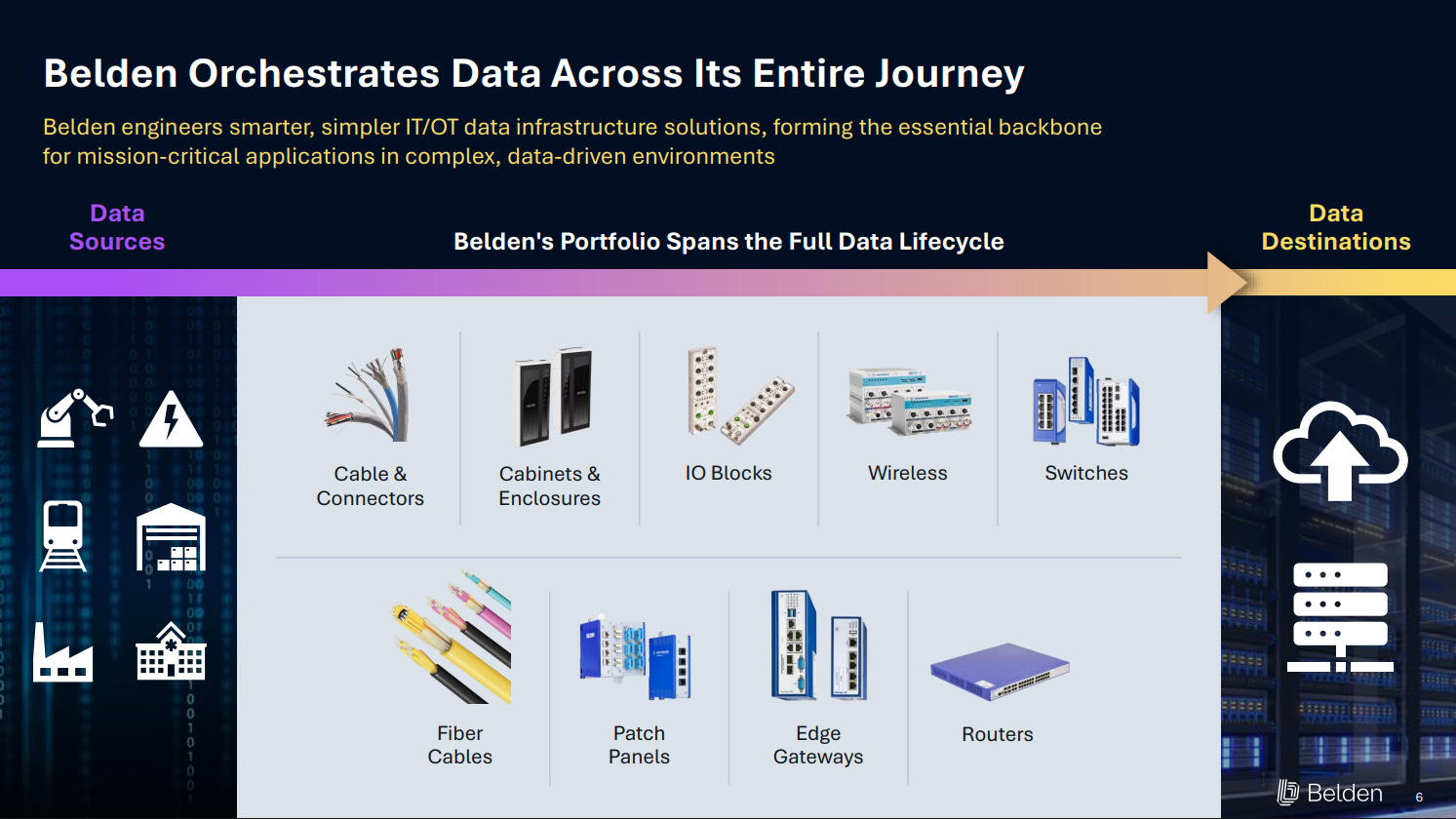

In simple terms, the company designs and manufactures the IT/OT networking infrastructure needed to move, secure and manage data across physical environments.

Automation Solutions sells rugged networking, connectors, software and cable into discrete automation, process automation, energy, transportation, warehousing, logistics and related industrial environments. Revenue grew +13.6% Y/Y in FY25 to $1.5B, reversing the declines seen in FY23 and FY24. Smart Buildings / Smart Infrastructure sells structured cabling, fiber and copper connectivity, racks, enclosures and active networking into data centers, healthcare, government, hospitality, commercial real estate and education. Revenue grew +7% Y/Y in FY25 to $586M, also reversing the prior two-year decline. Broadband serves broadband and wireless providers through brands such as PPC and Precision Optical, with revenue up +6% Y/Y in FY25 to $633M.

Belden is moving beyond component sales toward a solutions-driven model where customers buy integrated network architectures rather than individual products. This combines passive infrastructure, active hardware, consultative design, software, security and support into larger deployments. Belden Horizon adds the software layer by giving customers one interface for secure remote access, vLOTO-controlled machine approvals, automation tool connectivity, OT DataOps, edge application management, network orchestration and network health monitoring. Software turns Belden’s physical products into a managed IT/OT platform across secure access, machine data, edge applications, orchestration and network health.

Across the three core verticals, FY25 revenue came in at $2.7B, +10.3% Y/Y, reversing the declines seen in FY24 and FY23. Most revenue is recognized when control of goods transfers to the customer, while software and support revenue is recognized ratably over the contract term. The business is still short-cycle, with customers generally not contractually obligated to buy exclusively from Belden or purchase minimum volumes. The short-cycle exposure is part of why the market treats BDC like a cyclical component company, despite the mix shift underway.

Belden’s go-to-market strategy relies on a portfolio of specialized brands, including Belden, Hirschmann, Lumberg Automation, macmon, NetModule, PPC, Precision Optical Technologies, ProSoft Technology, Thinklogical, Tofino Security, CloudRail, Mohawk and West Penn Wire. Each brand addresses a specific part of the connectivity stack, creating a path to cross-sell as customers converge OT and IT networks. BDC uses a hybrid GTM model that combines direct consultative selling with a broad distribution network. Channel partners are the key route to market, but direct engagement is becoming more important as Belden sells more engineered solutions and gets specified earlier in customer designs.

Cable and wire can look commoditized from the outside, but Belden’s products are often engineered into environments where reliability, protocol compatibility, certification and installer familiarity drive purchasing decisions. This is especially true in industrial automation, data centers, broadband networks and regulated infrastructure. The company’s distribution model can be restrictive, but specification-led demand and a broad product portfolio help protect share. The U.S. accounts for 58% of revenue, with the remaining revenue spread globally.

Component manufacturing is lower-margin and exposed to input costs, especially copper, but Belden has historically passed through price increases with limited disruption. Gross margins have held in the 37%-38% range over the last three years, while FY25 operating margin was 11.6%. As the solutions mix rises along with acquisition synergies, management is targeting 25%-30% incremental adjusted EBITDA margins, supported by higher-margin active hardware, software, services and operating leverage.

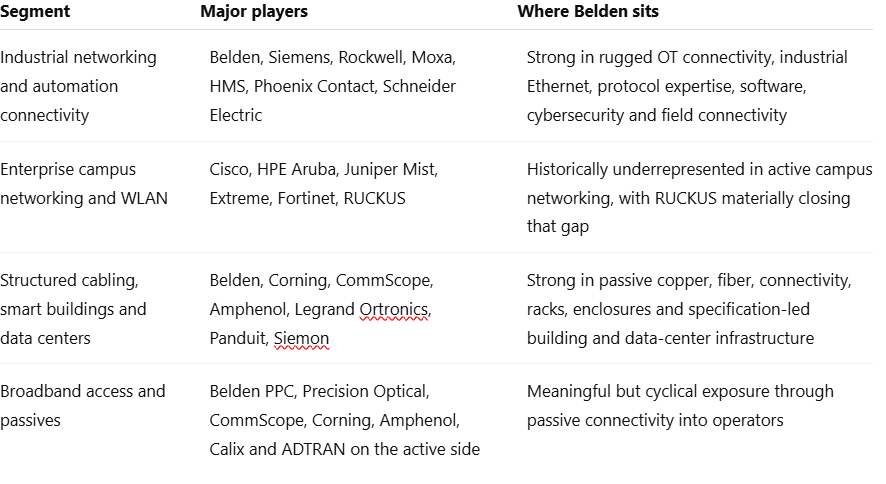

Belden operates across a fragmented set of adjacent markets spanning industrial networking, enterprise and campus networking, structured cabling and physical network infrastructure, and broadband access connectivity. Its moat is built on switching costs, application engineering, channel/specification power, breadth and scale. In industrial automation, downtime is costly, protocol compatibility matters and rewiring is painful. In smart buildings and structured cabling, specification-in, installer familiarity and certification drive share. In broadband, operators care about reliability, standards compliance and cost.

The Customer Innovation Centers support this strategy by bringing customers into the design process earlier and helping Belden move from discrete product sales to engineered solutions. This supports higher wallet share, better stickiness and a stronger margin profile.

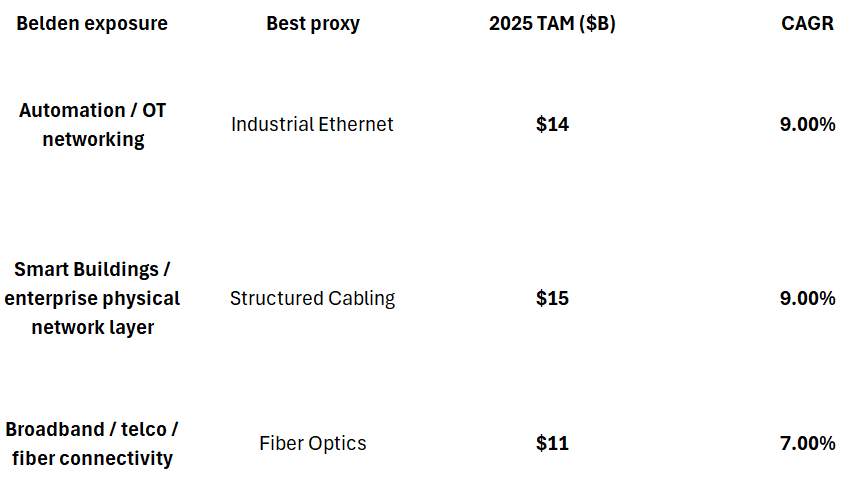

It is difficult to pinpoint a precise TAM given BDC’s broad exposure, but my estimate is that BDC currently serves a ~$40B serviceable TAM growing at an ~8% CAGR through 2035. Including RUCKUS, I believe the TAM expands to $50B-$60B.

Management’s capital allocation framework prioritizes organic reinvestment, strategic bolt-on M&A and shareholder returns. Belden completed 10 acquisitions during 2020-2025, deploying approximately $400M. The strategy culminated in the April 2026 announcement of the $1.85B RUCKUS Networks acquisition, which gives Belden the active wireless and switching layer needed to build a more complete IT/OT networking platform. With RUCKUS, management aims for solutions to reach 30% of total revenue by 2028, above the prior 20% target.

Belden has also returned more than $700M through repurchases since 2019, reducing the share count by more than 11% since 2021. Management historically targeted ~1.5x net leverage and reached that level in 2022 and 2023. The RUCKUS acquisition will raise leverage near term, shifting capital allocation toward deleveraging and temporarily pausing M&A and buybacks until leverage returns to target levels.

Belden is led by President and CEO Ashish Chand, who joined the company in 2002, and CFO Jeremy Parks, who has spent 15+ years in financial leadership roles at Belden. Management is aligned with shareholders through relative TSR, which represents 50% of PSU performance and is measured against the S&P 1500 Industrials Index over three years. Ownership requirements are also meaningful, with the CEO required to hold 6x base salary in Belden stock and other NEOs required to hold 3x. The 2025 PSU grants include a 1.5x share multiplier if adjusted EPS reaches $11.00 by 2028, tying long-term compensation to earnings growth and share price performance.

The core business thesis

BDC’s core business supports a large part of the thesis before assigning any value to RUCKUS and the “call options.”

Automation

In Automation, reindustrialization and reshoring are driving a multi-year need for industrial networking, rugged connectivity and secure plant-level data infrastructure. Manufacturing capacity is moving closer to the point of consumption, particularly in North America and Western Europe, and management has said that while customers may use different “friend-shoring” strategies, the reshoring element is a “100% definite yes.”

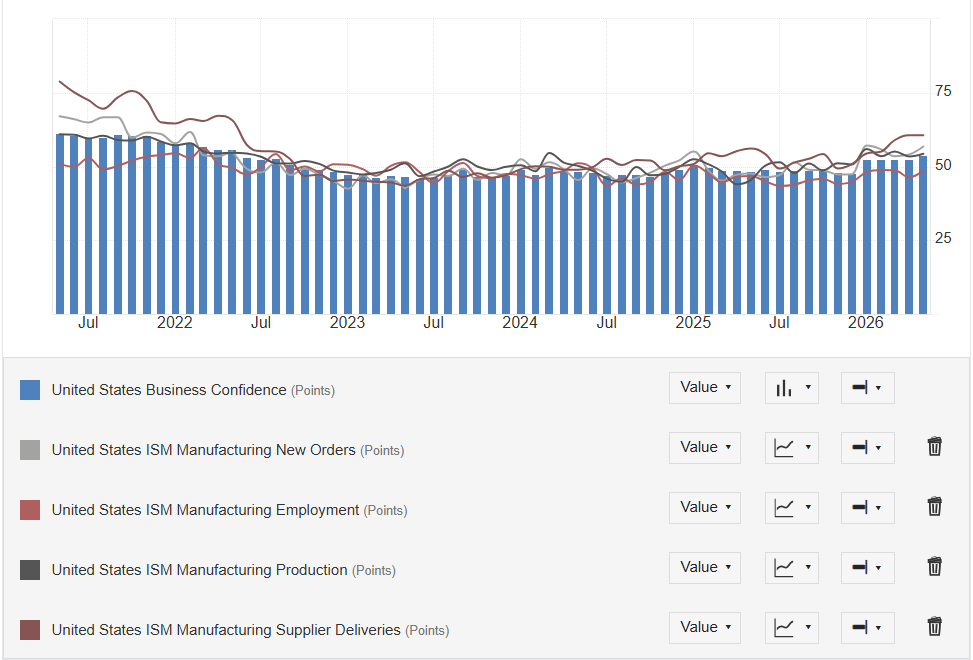

The macro data is beginning to support this view. After 3 years of contraction, the recent May ISM PMI reading of 54.0 marked the fifth straight month of expansion.

The important detail here is that Manufacturing Employment is the only major input still in contraction. For Belden, this is a favorable version of manufacturing recovery because production is coming back without the same recovery in labor availability, forcing manufacturers to increase automation intensity rather than rely on headcount.

7M manufacturing jobs have been lost over the past 15 years and are showing no signs of coming back. This means that the current “manufacturing renaissance” is decoupling production from human labor and shifting to automation.

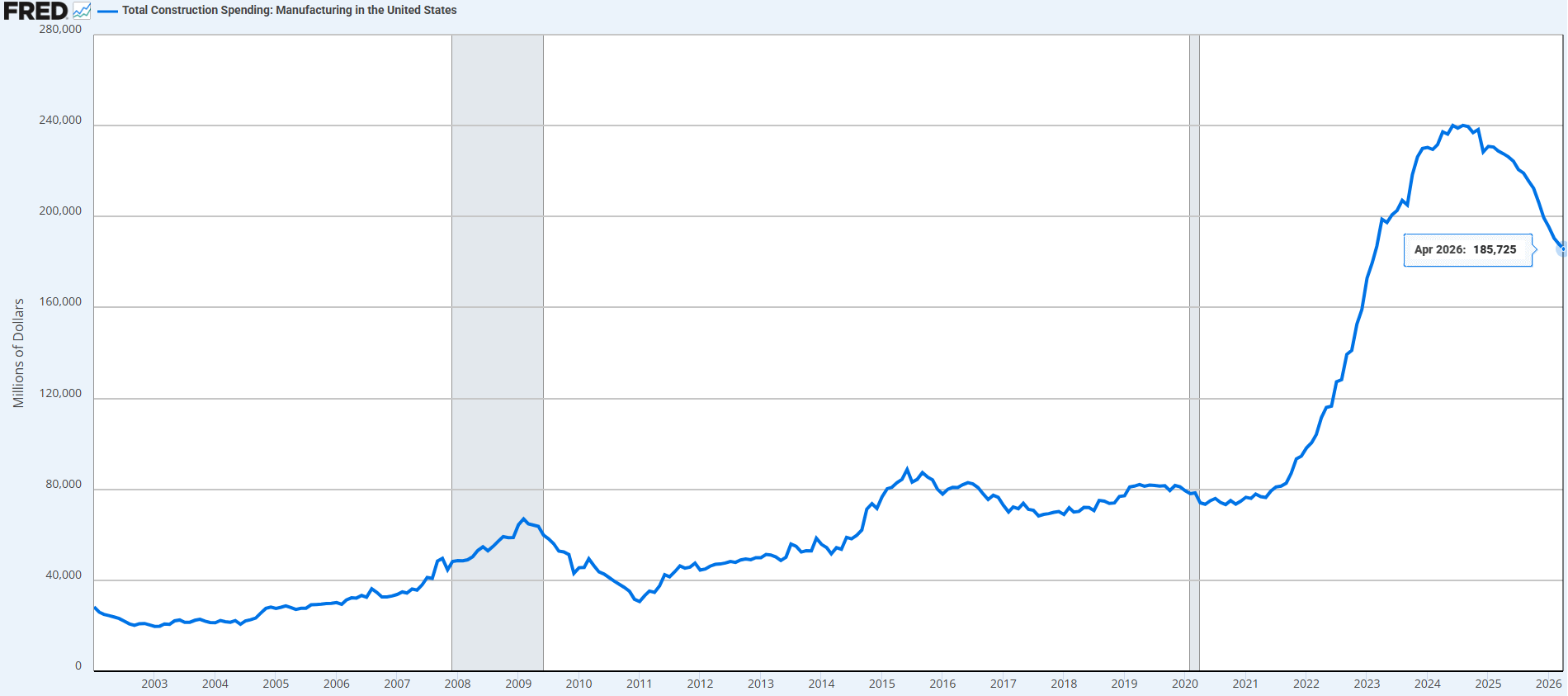

Factory starts alone are a poor proxy for Automation revenue. Belden participates later in the capex cycle, when projects move from site preparation and structural framing into mechanical, electrical, plumbing, controls, networking and commissioning. FRED’s TLMFGCONS data shows manufacturing construction spending peaked at ~$240B in 2024 and declined to $186B in the latest April 2026 reading. The initial surge was driven by CHIPS Act and IRA-related factory buildouts; the next phase is the plant infrastructure layer needed to make those facilities operational.

This multi-year pipeline of factory footprints requires industrial Ethernet, secure network architecture, ruggedized connectivity and IT/OT infrastructure. Management has pointed to this trend across customer verticals since early 2025, with pipeline strength in pharmaceuticals, consumer goods, logistics and automotive.

Labor scarcity is the second leg of the Automation thesis. Reshored facilities need to run with fewer skilled workers, which turns automation and digitized productivity into a requirement. Management has framed this directly, noting that inflation is pushing customers toward automation because the U.S. does not have enough workers to manufacture all the products being reshored. The answer is higher output per worker through automation.

Compounding this issue is the macroeconomic reality of an elevated cost of capital. Industrial players face a complex trilemma: they must expand domestic capacity, navigate a labor shortage, and optimize returns on expensive borrowed capital. The only viable solution to defend corporate margins is to sweat existing assets harder by amplifying output per square foot through extreme automation.

Automation organic revenue grew MSD in 1Q26, while reported revenue grew +10.6% Y/Y. FY26 growth may come in below FY25 because last year benefited from the destocking recovery, but the vertical is shifting from inventory normalization to a longer automation and network upgrade cycle.

Broadband

Broadband has been one of the main reasons investors view Belden as a short-cycle cyclical. This perception was reinforced during the 2023-2025 downturn, when the business was hit by customer inventory correction and pauses in network architecture upgrades.

The downturn had two main causes. First, broadband customers over-ordered after COVID to protect against supply chain issues, creating excess inventory across the channel. In 3Q23, Belden saw a sudden procurement shift as major MSOs moved from restocking to inventory reduction and shorter lead times, driving a 28% sequential drop in orders. Second, deployments slowed in the back half of 2025 as MSOs dealt with technical interoperability issues across complex DOCSIS upgrade stacks, creating stops and starts in project execution.

By late 2025, customer inventory levels had moved back toward longer-term norms, and management confirmed in early 2026 that the correction phase was over. 1Q26 Broadband revenue grew +5.9% Y/Y despite lapping a +31% comp in 1Q25 and despite 1Q being seasonally slower. Management also expects improvement through the rest of 2026.

Belden is now entering a structural growth phase driven by a multi-year upgrade cycle for higher speeds and increased fiber density. Broadband has shifted away from bulk fiber and commodity cable volume toward higher-value access fiber and last-mile network upgrades. Fiber has grown from ~5% of Broadband revenue five years ago to ~50% today, with Belden focused on higher-finesse access fiber rather than lower-value trunking.

Aside from the cyclical recovery and shift in fiber, a significant catalyst for the Broadband business is the BEAD catalyst. The $42.45B Broadband Equity, Access, and Deployment program is the largest broadband infrastructure stimulus in U.S. history. With state allocations approved and field construction beginning, capital deployment should scale through the end of the decade. Belden is positioned to capture this spend because the leading BEAD recipients overlap with its largest long-standing MSO accounts. After the inventory correction, BEAD creates a multi-year demand layer on top of the fiber and DOCSIS upgrade cycle.

Smart Buildings

Do not let the networking label fool you; Belden is not a pure data center networking play. Data centers make up less than 20% of Smart Buildings revenue. Instead, this segment is a play on institutional property upgrades and data center “gray space”.

The segment was historically viewed as a proxy for non-residential construction and corporate office, but CRE now accounts for less than 10% of vertical revenue. Capital and engineering resources have shifted toward healthcare networks, hospitality campuses, education, high-density venues, data centers and localized enterprise edge installations.

Demand is increasingly tied to brownfield retrofits, regulatory pressure and operating efficiency. Hospitals, hotels, campuses and venues are upgrading existing infrastructure to automate workflows, improve security, manage energy usage and consolidate fragmented systems onto one backbone. This type of capex is less dependent on new physical square footage and more tied to the need to modernize existing assets.

Belden’s data center exposure is also more attractive than the headline mix suggests. The company focuses on gray space infrastructure, including facility power management, substation automation, building controls, security, specialized climate systems and liquid cooling networks needed to keep high-density AI clusters online. It avoids the most commoditized white space applications, including standard compute racks and high-volume cabling where pricing pressure is much higher.

A primary proof point is the 2Q25 multi-site solutions award with a tier-1 AI hyperscaler, where Belden is installing ruggedized industrial networking products across advanced cooling systems. Power and cooling availability are becoming the major bottlenecks for AI infrastructure, and those bottlenecks require the industrial-grade networking and control infrastructure Belden already sells.

Reported data center exposure likely understates the true revenue base because a portion of racks, wire and cable is sold through distributors that ultimately serve data center customers. Management has expanded the dedicated data center team by 2-3x over the last few quarters and disclosed that the active data center solutions pipeline is roughly 2x to 4x the current realized revenue base.

Solutions mix in the vertical was effectively 0% at the start of 2025 and reached a MSD % by 1Q26. As Belden moves toward its company-wide solutions target, Smart Buildings should see one of the stronger margin ramps because the offering increasingly combines active hardware, passive infrastructure, software and services.

The inflection already started to show in 1Q26, with Smart Buildings revenue up +21% Y/Y, aided by an easier comp and double-digit growth in data center-related revenue. FY26 growth should outpace the +7.4% seen in FY25 if retrofit demand stays healthy and data center gray space continues to scale.

The Solutions Transformation and a Unified Model

Industry experts have characterized Belden’s distribution as “very restrictive,” particularly in wire and cable, noting that Belden often limits direct access to a small number of approved partners to protect its highly specified “Belden Classics” products. This model has historically led to crossovers where unapproved distributors switch a Belden specification to a competitor’s product because they cannot procure Belden directly. This strategy is what has been putting a lid on top-line growth.

The unified operating model is designed to fix this constraint. Management has acknowledged that the prior segment structure created internal walls and limited cross-selling. The new model creates a single customer-facing structure and allows Belden to sell enterprise, broadband and industrial products through key distribution partners with a more complete view of the customer’s network needs.

CEO Ashish Chand noted that reaching a 15% solutions mix by 2025 involved “a little bit of brute force” because the company was not organized to service customers on a unified basis. The realignment is designed to move Belden from bespoke, one-off designs to scalable reference architectures that can be easily adopted across the entire channel. Management is focused on a balance of simplifying complex solutions so customers can adopt them more easily, which they believe will cause “adoption rates to go up dramatically”.

This move plays directly into ramping the solutions business, which in effect realizes higher revenue due to the bundling of products and services, as well as higher margins with a better mix of products including software and the ability to skip the distributor by selling to the end-consumer.

Belden has deployed over 250 solutions consultants who work directly with end-users to specify Belden products into their designs. Once specified at the design level, the high-margin active products (switches, software) automatically pull through high volumes of traditional passive products like cabling, regardless of which distributor fulfills the order.

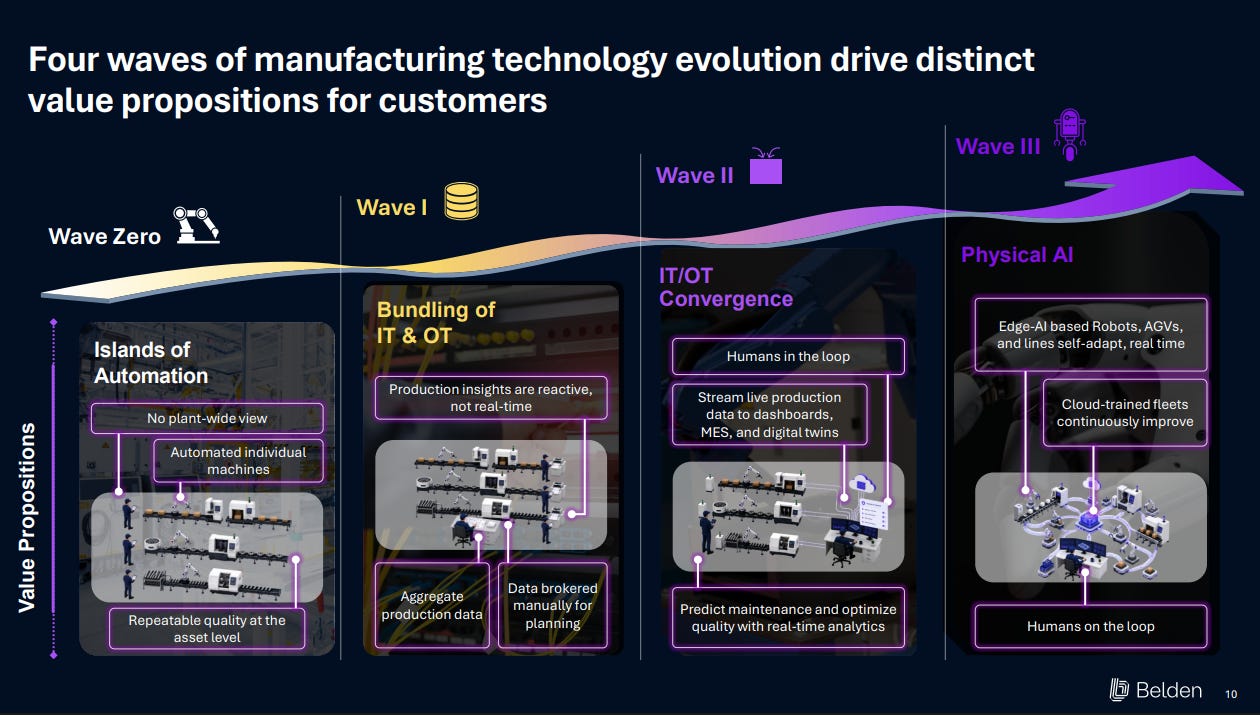

IT/OT Convergence

IT/OT convergence is one of Belden’s most important growth drivers. Historically, enterprise IT networks and plant-floor OT networks operated separately. IT handled enterprise data, email, ERP systems and cloud applications, while OT controlled machines, sensors, assembly lines and physical processes through fragmented legacy protocols such as Modbus and Profibus.

Factories, warehouses, hospitals, utilities and transit systems now need real-time data moving securely between physical assets, edge devices, control systems and enterprise software. Without a converged IT/OT network, Physical AI, autonomy, predictive maintenance and edge computing cannot function at scale. A robot, grid asset or automated warehouse system cannot self-adjust in real time if the data is trapped inside isolated systems or routed through slow, fragmented networks.

This expands Belden’s wallet share. In a siloed network, Belden may only sell the passive layer, including cable, connectors and physical infrastructure. In a converged architecture, Belden can sell the full stack, including ruggedized switches, edge devices, security, network management software and data orchestration. A project that may have been limited to raw cable volume can become a larger engineered solution across the full data journey, from sensor capture to edge processing to secure cloud connectivity.

RUCKUS causing a Ruckus, the good kind

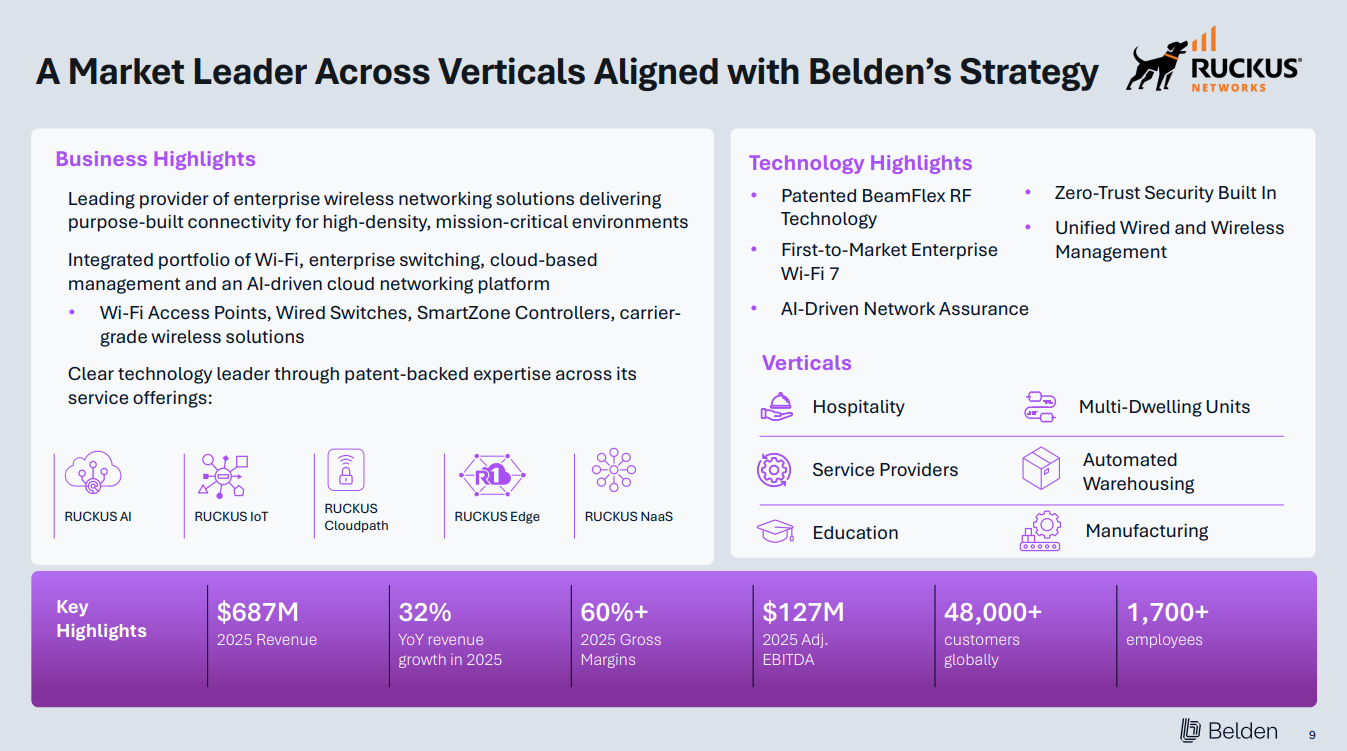

The RUCKUS acquisition is being priced as an overhang even though it accelerates Belden’s solutions transition. Leverage moves higher, but Belden also gains a faster-growing, higher-margin active networking asset with 48K+ customers, 32% Y/Y revenue growth in 2025, 60%+ gross margins and projected adjusted EBITDA margins above 20% in the first full year of ownership. At ~13x projected 2026 adjusted EBITDA, RUCKUS lifts the pro forma solutions mix from 15% to over 20%, pushes consolidated gross margins above 40% in 2026 and takes the combined EBITDA base to ~$650M with $360M+ of unlevered FCF.

Belden has recently secured $1.85B of debt financing from JPM at SOFR + 225 bps. The market is focused on the headline multiple and leverage step-up, while underweighting the asset quality and cross-sell opportunity inside Belden’s installed base.

Part of the skepticism comes from RUCKUS changing hands five times since 2016, from Brocade to Arris to CommScope to Vistance to Belden. The history can look like product weakness, while the better explanation is market timing, parent-company balance sheet pressure and a product portfolio better suited as part of a broader networking platform. RUCKUS was repeatedly caught inside parent companies with different strategic priorities.

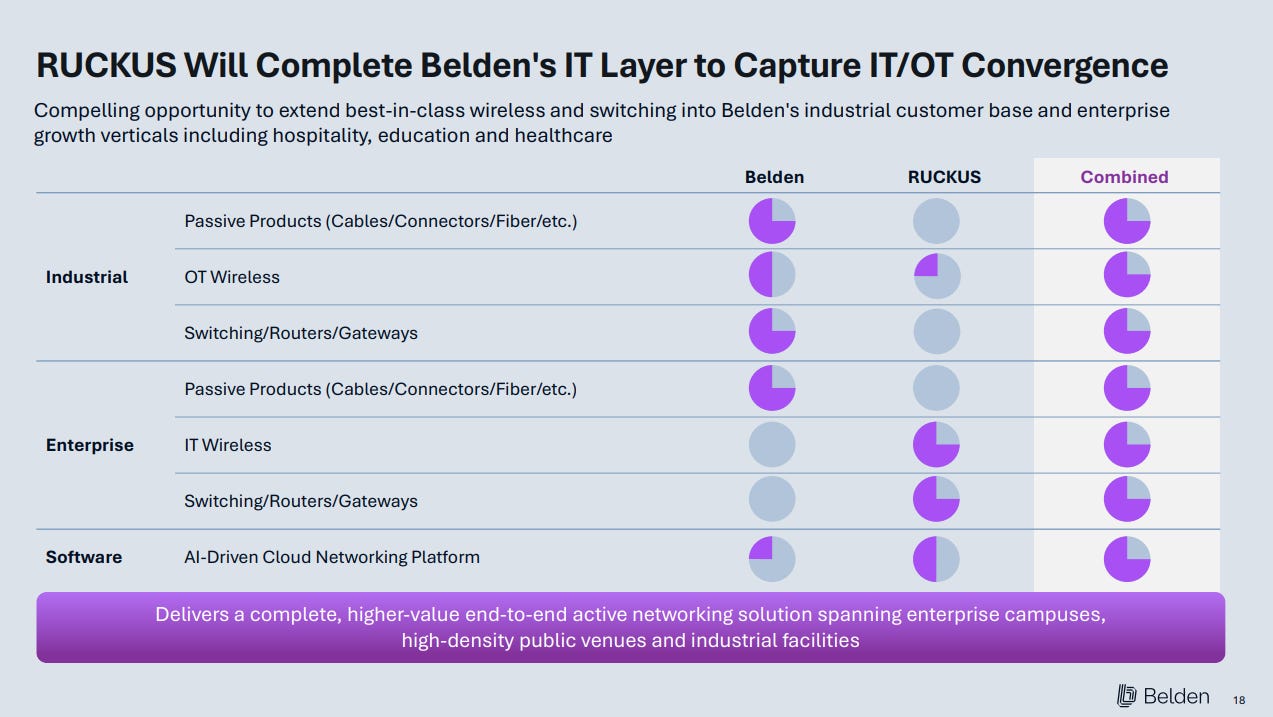

The strategic limitation of RUCKUS as an independent asset is specialization. Its ICX switching line adds campus switching, but the portfolio lacks the broader enterprise stack of Cisco or HPE, including campus core switching, data center routing, SD-WAN, AI-driven security and unified licensing. Large enterprise buyers often prefer a single vendor across the network stack, which has left RUCKUS treated as a high-quality Wi-Fi point solution.

This is EXACTLY what a combination with Belden solves.

Belden gives RUCKUS the horizontal context it lacked. Belden already owns passive infrastructure, industrial connectivity, OT security, customer specifications and distribution reach. Adding RUCKUS gives Belden the active wireless and switching layer needed to offer a more complete active and passive network architecture from the industrial edge to the enterprise campus.

RUCKUS was first-to-market with enterprise Wi-Fi 7 through the R770 access point, placing the business at the front end of a multi-year upgrade cycle as enterprise networks move toward higher density, lower latency and more deterministic wireless. Peer commentary across networking already points to rapid Wi-Fi 7 adoption, with HPE citing +600% growth in Wi-Fi 7 sales from network modernization. RUCKUS also adds RUCKUS AI, an AI-driven cloud networking platform for assurance and optimization, along with a more advanced NaaS offering than Belden had on its own.

RUCKUS is primarily enterprise today, with hospitality and education as its two largest verticals. It also has exposure in automated warehouses and material handling, already overlapping with Belden’s industrial base. The overlap creates the first layer of synergy. Belden can combine its passive infrastructure with RUCKUS’ active wireless and switching portfolio on the enterprise side, while taking RUCKUS deeper into legacy industrial markets where wireless adoption is still early.

Discrete manufacturing offers the largest upside because most machine data still moves over wireline networks, while management expects wireless to move toward a 50/50 mix over the next 3-5 years and potentially become the majority of machine data traffic over time. Customers are already planning for the shift, but many lack one vendor capable of providing the full blueprint across passive infrastructure, ruggedized networking, enterprise wireless, cybersecurity and software management. With RUCKUS, Belden can become the blueprint vendor.

Across Automation, Smart Buildings and Broadband, RUCKUS adds capabilities directly tied to Belden’s existing vertical strategy. In Automation, it extends high-performance wireless into industrial environments needing low-latency connectivity for Physical AI, robotics, autonomy and machine-to-cloud data flows. In Smart Buildings, it completes the IT layer for healthcare, hospitality, education and large campus environments, moving Belden beyond fixed infrastructure into mobile, reliable hybrid networks. In Broadband, it brings carrier-grade wireless, 4G/5G and service-provider exposure, strengthening Belden’s ability to deliver integrated networks across campuses, venues and smart cities.

By 2028, management expects RUCKUS to help push solutions mix to 30% of total revenue. The importance of the acquisition is not only the revenue contribution, but the change in what Belden can sell. Belden moves from a strong passive and OT-facing supplier into a more complete active and passive networking provider with higher wallet share, stronger margins and a better position in the IT/OT convergence cycle.

Wireless networking upgrade cycles generally span 5-6 years. The shift from Wi-Fi 5 to Wi-Fi 6 lasted ~5-6 years from initial ratification to enterprise saturation. Wi-Fi 7, formally certified by the Wi-Fi Alliance in January 2024, should drive a 6-7 year enterprise upgrade cycle peaking around 2030-2031.

IDC data shows Wi-Fi 7 moving from less than 1% of enterprise dependent AP revenue in 1Q24 to 44.5% by 1Q26, making it one of the fastest-ramping enterprise wireless standards in its tracking. Adoption is being pulled forward by a maturing Wi-Fi 6/6E installed base, AI-powered enterprise applications with higher throughput and latency requirements, and broader availability of certified access points across price tiers. Wi-Fi 7’s Multi-Link Operation and 320 MHz channel support address these requirements directly, which is pulling forward buying decisions previously expected in 2027 or later.

Management expects HSD growth in 2026 from RUCKUS’ $687M 2025 revenue base, but the outlook appears conservative. Vistance WLAN revenue grew +12.9% Y/Y in 1Q26 before the asset was sold, while industry research points to 60%+ Y/Y Wi-Fi 7 market growth in 2026 and a 25%+ CAGR over the next 3-5 years. RUCKUS has MSD share behind Cisco and HPE, so share stability or share capture can drive growth above expectations.

Call Options

Physical AI

As AI moves into robotics and automation, Physical AI gives Belden another upside path beyond the core automation cycle. The global Physical AI market is estimated at $5.4B in 2025 and is expected to reach ~$61.2B by 2034, implying a 31.3% CAGR. Belden does not need to pick the winning robot, sensor stack or AI model. Its role is to provide the local network infrastructure required for these systems to operate safely and reliably.

Physical AI shifts machinery from fixed automation to adaptive real-world decision-making. Humanoid robots, computer-vision picking systems and autonomous mobile robots require uninterrupted telemetry from cameras, LiDAR, sensors and force-feedback loops. These assets make constant mechanical adjustments based on real-time inference, so packet loss, jitter or latency can cause immediate physical failure, including machine collisions, missed picks or dropped freight.

Industrial facilities deploying these systems need more than standard connectivity. They need active infrastructure capable of Time-Sensitive Networking, deterministic data movement and plant-wide clock synchronization. This pushes customers from basic cable and connector purchases toward full IT/OT solutions, including OpEdge hardware, industrial firewalls, ruggedized switches and Belden Horizon for data orchestration. The same factory footprint can shift from passive products carrying ~37% gross margins to solutions wins with gross margins above 50%.

Physical AI therefore expands Belden’s wallet share while limiting platform-specific risk. Whether the winning system comes from a robot OEM, warehouse automation vendor or industrial software company, the facility still needs a secure, low-latency network layer underneath it. Belden gets paid on the infrastructure required to make the physical AI deployment work.

Edge Computing and Localized Inference

Edge computing moves processing and storage closer to the data source, while localized inference runs AI models directly on local devices. The need is simple: industrial customers cannot send every machine-data stream to the cloud, wait for processing, then route the answer back to the plant floor. Management has already called this “super expensive,” and safety-critical environments require microsecond decision-making with local control.

Token costs, bandwidth limits and open-source model restrictions should also push more inference toward the device or local edge server. Research estimates the global edge computing market will reach $140B by 2030, implying a 32% CAGR, while Edge AI is projected to grow at a 21% CAGR as connected devices scale toward a projected 1T IoT connections by 2030.

Belden is positioned to benefit through both hardware and software. On the hardware side, the company provides ruggedized switches, gateways and time-sensitive networking infrastructure required to move machine data locally with low latency. On the software side, Horizon acts as the orchestration layer for edge devices, allowing customers to run containerized applications, detect anomalies locally and manage distributed edge networks without routing every decision through the cloud.

The edge opportunity reinforces the same core shift across Belden’s business. More data created at the machine level means more need for secure connectivity, local processing, network orchestration and software-enabled infrastructure.

Revenue Build

Management’s long-term target is MSD annual revenue growth, or 4%-6%. In my view, this is conservative and does not reflect the revenue opportunity over the next 2-3 years. There is far more upside than downside given the drivers across the core business, RUCKUS and the call options.

Consensus is even more conservative, projecting +4.6% revenue growth in 2027 and +3.8% in 2028. Either estimates have not been updated for RUCKUS, or the sell-side is waiting for the deal to close before fully reflecting the pro forma revenue base.

The RUCKUS acquisition is expected to close in 2H26. Financing has been secured, leaving regulatory approvals as the primary remaining step, which I expect to clear given the size and structure of the industry. Assuming a 4Q26 close, BDC would receive one quarter of RUCKUS contribution. Management expects HSD growth from RUCKUS’ $687M 2025 revenue base. Using +8% Y/Y growth implies ~$742M of annualized revenue, or ~$185M per quarter. I use $180M to account for seasonality, with 2Q and 3Q typically stronger.

From what I see, FY26 consensus may not be fully updated for RUCKUS, or it may simply be overly conservative on the core. FY26 consensus revenue is $2.97B, +9.4% Y/Y. If consensus includes one quarter of RUCKUS, or ~$180M, implied BDC-only growth is just +2.7% Y/Y. Unless the sell-side is seeing something I am not, this looks too low for a business coming out of destocking with improving demand across all three verticals.

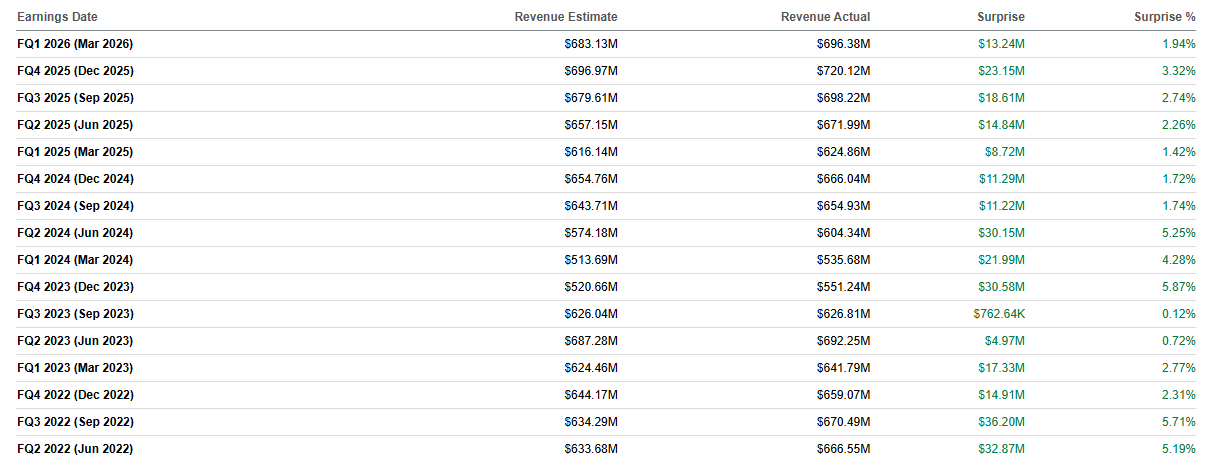

Under the assumption consensus is still BDC-only, the 2027 and 2028 numbers look even more disconnected. Consensus projects +4.8% Y/Y growth in 2027 and +3.6% Y/Y in 2028. In my view, this is too low for a business in cyclical recovery with ramping exposure to automation, data center gray space, broadband upgrades and RUCKUS cross-sell. Consensus appears anchored to the post-COVID supply glut and destocking period, while also leaning heavily on management’s conservative long-term algorithm. As shown below, management has beaten top-line consensus estimates in each of the past 16 quarters.

The next 2-3 years should look very different from 2023-2025. Industrial customers need to automate in response to reindustrialization, inflation and labor scarcity. Smart Buildings customers need to retrofit facilities for IT/OT convergence, energy efficiency, security and data center gray space. Broadband is entering a multi-year upgrade cycle with BEAD as a funding catalyst. RUCKUS adds an obvious cross-sell opportunity across Belden’s enterprise and industrial customer base, while Physical AI, edge computing and localized inference provide upside beyond the base case.

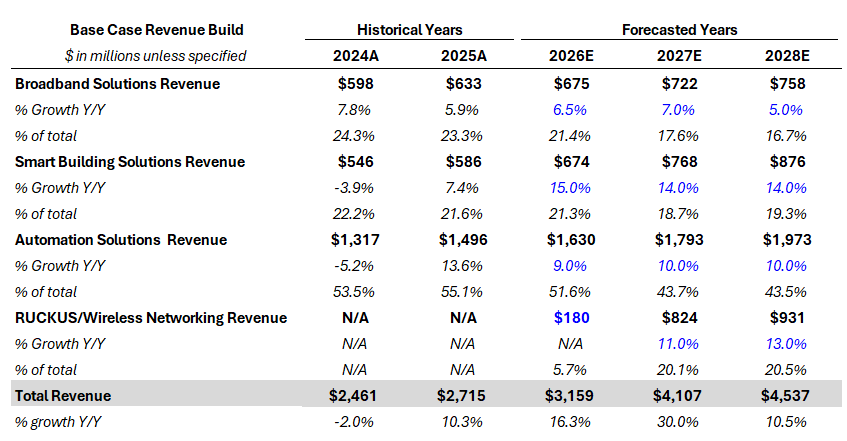

My assumption is RUCKUS will be broken out as a separate business line under wireless networking. For the BDC core business, I model revenue growth of +10.4% Y/Y in 2026, +10.2% Y/Y in 2027 and +9.8% Y/Y in 2028, implying a 9.92% CAGR over the 2026-2028 forecast period.

Across the three core verticals, I project a 3-year CAGR of 9.7% in Automation, with growth ramping in 2027 and 2028. In Broadband, I project a 3-year CAGR of 6.2%, with growth highest in 2027 as BEAD begins to scale. In Smart Buildings, I project a 3-year CAGR of 14.3%, driven by retrofits, data center gray space and solutions mix.

This marks a sharp contrast to the cyclical irregularity seen in 2023-2025, when average growth was 4.7%. The market is still underwriting the last cycle, but supply is no longer overbuilt and demand is improving across all three verticals.

For RUCKUS, I assume management’s conservative HSD 2026 growth expectation holds. In 2027, I project growth of 11%+ Y/Y as cross-selling across BDC’s industrial and enterprise base starts to take effect. In 2028, I project +13% Y/Y, reflecting further cross-sell ramp and the solutions transformation moving closer to management’s 30% mix target.

All in, revenue inclusive of RUCKUS comes out to $3.16B in FY26E, +16.3% Y/Y, $4.1B in FY27E, +30% Y/Y, and $4.5B in FY28E, +10.5% Y/Y. This implies a 2026-2028 CAGR of +18.7%.

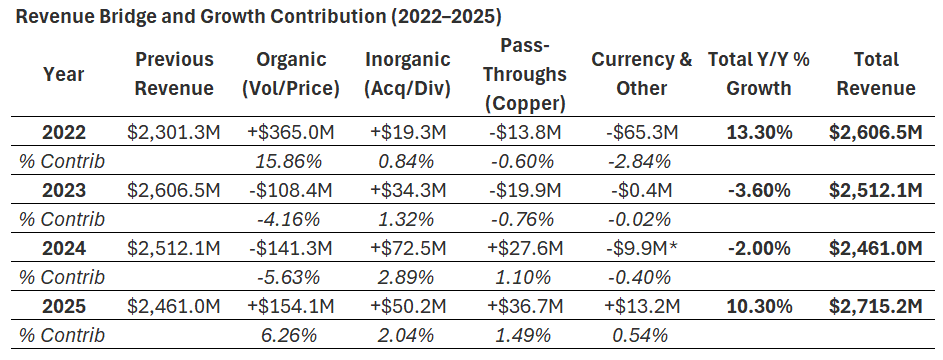

A smart reader like yourself could point to pass-throughs and FX, but these have contributed at most ~2% over the past four years, including 2025. The disconnect is not copper, FX or one-off pricing. The issue is a likely misunderstanding of where the underlying verticals are in their cycles.

Margin Thesis and EBITDA Build

BDC’s margin thesis rests on mix, pricing, operating leverage and RUCKUS. IT/OT convergence is accelerating the solutions transformation because customers are buying integrated architectures across passive hardware, active hardware, software and services, rather than standalone cable, connectors or basic components.

Traditional product sales, including wire, cable and basic connectors, typically generate gross margins in the 36%-37% range. These products are often sold through distributors and contractors and carry more unit-price competition. Full solution sales, which combine passive products with active components like switches, routers and gateways, plus software such as Belden Horizon, typically command gross margins in the 50% range.

The shift also changes the pricing discussion. BDC engages with customers through a consultative process tied to operating KPIs, such as reducing plant scrap or improving hospital safety. This gives Belden more room for value-based pricing instead of competing through RFPs based mainly on unit price.

Expert calls have validated Belden product quality as best-in-class, reinforcing a TCO-over-price purchasing framework. Customers increasingly evaluate Belden’s solutions based on productivity gains and lifecycle savings, reducing price pressure even in inflationary environments.

Management targets 25%-30% incremental adjusted EBITDA margins, which translates to 50-75 bps of annual gross margin improvement plus operating leverage across SG&A and R&D.

RUCKUS adds a higher-margin asset to an already improving core. RUCKUS generates gross margins above 60% and should push consolidated gross margins to ~40% immediately post-close. RUCKUS also generates adjusted EBITDA margins above 20%, compared with Belden’s 16.9% adjusted EBITDA margin in FY25. The combination accelerates the solutions mix toward 30% of revenue by FY28. Belden also gains scale synergies from selling RUCKUS into its industrial customer base, while durable Wi-Fi 7 demand should limit pricing pressure for at least the next few years.

In my view, consolidated GAAP gross margins expand 445 bps over the next 3 years, with most of the improvement driven by RUCKUS integration. I assume RUCKUS gross margins hold steady at 61%, in line with management’s comment, “RUCKUS consistently delivers gross margins above 60%.” For the core business, I model 67 bps of expansion in Smart Infrastructure, including Broadband and Smart Buildings, and 25 bps in Automation. Most consolidated gross margin expansion arrives in 2027, the first full year of RUCKUS ownership.

EBITDA margins should inflect under the unified model and RUCKUS combination. I model 473 bps of EBITDA margin expansion over the next 3 years (458 bps of adjusted EBITDA margin expansion), with most of the improvement in 2027. This aligns with management’s expectation for 20%+ RUCKUS adjusted EBITDA margins in the first full year of ownership and its 25%-30% incremental adjusted EBITDA margin target.

Valuation and Risks

Due to the overhangs mentioned above and Belden’s “industrial” label, the stock has consistently traded at a discount to networking peers. This has also reinforced consensus conservatism. As they say, price drives sentiment.

The acquisition overhang is turning into a catalyst, while Belden’s industrial label, which capped the multiple during the post-COVID destocking cycle, should begin to help as reindustrialization and upgrade cycles accelerate. An inflecting core business, revenue and margin upside, RUCKUS synergies, the industrial + networking + AI thematic, likely beats versus stale consensus estimates, and the call options from Physical AI, localized inference and edge computing create a setup for multiple expansion.

BDC currently trades at a steep 10.3x EBITDA discount versus the mean of the comp set on consensus forward estimates. Even after accounting for the new leverage, assuming the full $1.85B was borrowed as of 1Q26, P14’s FY26E EV/EBITDA estimate is ~14.5x, still a considerable discount versus the comp set mean of 21.4x.

If the P14 base case is executed, I think BDC trades at 15x 2027 EBITDA at some point within the next two years. The likely catalysts are earnings upside versus consensus, a reflexive move in price driving sentiment, and a broader rotation toward industrial automation and Physical AI. Once the market realizes 2026-2028 does not look like the post-COVID 2023-2025 period, the multiple should re-rate closer to peers.

With the new debt raise, principal debt would be ~$3.1B assuming no repayments. Using management’s 2.9x net leverage target by 2027, net debt would decline to ~$2.6B. Assuming a steady share count, the P14 base case PT on 15x FY27E EBITDA is $235/sh, or +93% from current levels, to be achieved in under two years.

Risks

Unlike high-multiple networking stocks caught in the momentum trade, Belden offers relative value in a market where momentum can unwind quickly. The multiple has more room to expand in response to earnings upside and catalysts, while the lower starting valuation should provide better downside protection in a sector-wide selloff. In a bear case, I see ~20% downside to $100/sh.

Quick rise in copper prices - A parabolic rise in copper would create an initial margin headwind before pricing actions flow through. Belden can pass through price increases with relative ease, but a rapid move in copper typically pressures margins near term. I do not expect a parabolic move given the strengthening dollar.

Macro/rates - BDC’s customers are capex intensive and sensitive to rates. A rate hike would pressure customer spending and increase BDC’s interest expense given the SOFR-linked debt financing. This would also weigh on the stock because leverage is one of the current overhangs.

Integration risk - Management has a strong capital allocation track record, and RUCKUS has clear synergies with BDC’s core business. Still, integration risk needs to be monitored because failure to execute would weaken one of the main drivers of the margin thesis.

No repurchases - Share repurchases will be temporarily paused until deleveraging targets are met. This removes an incremental buyer of shares near term, but projected FCF growth from the core business and RUCKUS’ high FCF conversion could allow buybacks to return in 2027.

Conclusion

Belden is a market leader across verticals entering a growth and margin inflection, with a highly accretive acquisition being priced as an overhang. The market and consensus are still stuck in the cloudy past while missing the bright green skies ahead. I am long with a core position at $112/sh.

Great write-up man! I am actually in the midst of posting an idea on BDC as well. I would love to talk to you about this idea if you're open to it!